Most SaaS founders obsess over ARR. They celebrate new logo wins and show board slides with 100% year-over-year revenue growth. But here’s the uncomfortable truth: ARR tells you almost nothing about whether your business is actually healthy. What matters is what happens after the sale — whether customers stay, expand, and become more valuable over time. That’s where Net Revenue Retention comes in, and once you understand it, you’ll never look at your metrics dashboard the same way again.

Net Revenue Retention (NRR) measures the percentage of recurring revenue you retain from existing customers over a given period, accounting for upgrades, downgrades, cancellations, and churn. Unlike simple retention metrics, NRR captures the full picture: a 100% NRR means your existing customer base is generating exactly the same revenue this period as they did last period, even if some customers left — as long as others expanded their spending to compensate. Any NRR above 100% represents pure expansion revenue, the kind that drives compounding growth without requiring proportionally more sales spend.

This article breaks down exactly how NRR works, why it matters more than any other SaaS metric, how it differs from Gross Revenue Retention, and what you can actually do to improve it. I’ll also share where conventional wisdom gets this wrong, because most SaaS articles treat NRR as a simple north-star metric without acknowledging its genuine limitations.

What Is Net Revenue Retention?

Net Revenue Retention is the percentage of recurring revenue retained from existing customers over a specific time period, including expansion revenue from upsells and cross-sells, minus revenue lost from cancellations and downgrades. It’s typically measured monthly, quarterly, or annually, and it paints a precise picture of how your existing customer base is evolving.

The NRR formula looks like this:

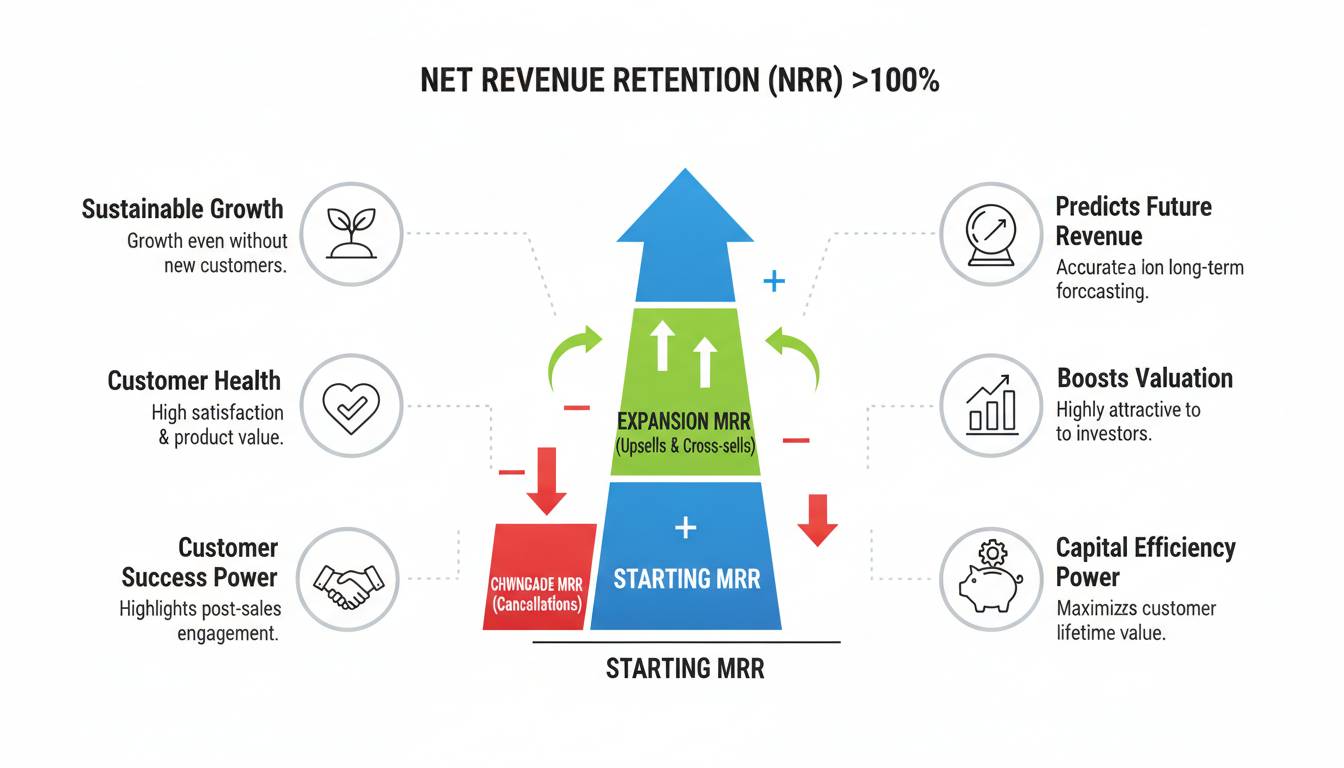

NRR = (Starting MRR + Expansion MRR – Contraction MRR – Churned MRR) / Starting MRR × 100

Here’s what each piece means:

- Starting MRR: The monthly recurring revenue from your customer base at the beginning of the measurement period

- Expansion MRR: Additional revenue from existing customers through upsells, new seats, upgraded plans, or add-on purchases

- Contraction MRR: Revenue lost from existing customers who downgraded their plans or reduced their usage

- Churned MRR: Revenue lost from customers who cancelled entirely

The key insight here is that NRR can exceed 100%. When your expansion revenue exceeds your contraction and churn combined, you have negative net churn — a phenomenon that top-performing SaaS companies achieve and one that creates the “land and expand” dynamics investors love.

A Concrete Example

Imagine you start Q1 with $1,000,000 in MRR. During the quarter:

- Existing customers upgrade, adding $150,000 in expansion MRR

- Some customers downgrade plans, losing $40,000 in contraction MRR

- Several customers cancel, losing $60,000 in churned MRR

Your calculation: ($1,000,000 + $150,000 – $40,000 – $60,000) / $1,000,000 × 100 = 105%

You retained 105% of your starting revenue from your existing customer base. You lost some customers, but the ones who stayed and expanded more than made up for it. That’s the magic of high NRR — your existing customers become a growth engine rather than a decaying asset that requires constant replacement.

Net Revenue Retention vs. Gross Revenue Retention

If NRR tells you the full story, Gross Revenue Retention (GRR) tells you an incomplete one. Understanding the difference is crucial, because many SaaS founders conflate the two and miss the actual health signal their business is sending.

Gross Revenue Retention measures the percentage of recurring revenue you retain from existing customers, excluding any expansion revenue. The formula is:

GRR = (Starting MRR – Contraction MRR – Churned MRR) / Starting MRR × 100

Using the same example above, GRR would be: ($1,000,000 – $40,000 – $60,000) / $1,000,000 × 100 = 90%

GRR can never exceed 100%. It answers a simple question: “If no existing customer spent another dollar with us, what percentage of their current revenue would we lose?” It measures pure retention, the baseline stickiness of your product.

NRR answers a different question: “What is the total financial value we’re extracting from our existing customer relationships, including everything they’re choosing to spend more on?”

The gap between your NRR and GRR reveals your expansion engine. If you have 90% GRR but 120% NRR, your expansion revenue ($150,000 in the example) more than compensates for your churn and contraction. You’re growing from within your existing base. That’s the difference between a business that must constantly acquire new customers to survive and one that compounds from its installed base.

Here’s where most articles get it wrong: GRR isn’t “worse” than NRR. They measure different things. A company with 100% GRR and 90% NRR has serious problems — customers aren’t expanding and are actually downgrading despite using the product. A company with 85% GRR and 140% NRR might have aggressive expansion tactics that are unsustainable. You need both metrics to understand what’s actually happening.

What Is a Good Net Revenue Retention Rate?

Benchmarks vary by company stage, segment, and business model, but industry data provides useful reference points. According to data from SaaS capital firms and analytics platforms, here’s how NRR typically breaks down:

Below 100%: Your business is in decay. You must acquire new revenue faster than existing customers are leaving or shrinking. This is sustainable only at the earliest stages when you’re rapidly adding new logos, but it becomes a serious problem as you mature and customer acquisition costs rise.

100-110%: You have basic retention but no expansion. This is a survivable zone but not a growth zone. You’re replacing churned revenue with new customer revenue, which works but requires consistent sales and marketing investment.

110-120%: You have a healthy expansion engine. Customers are staying and spending more. This is the typical range for well-performing mid-market SaaS companies.

120-140%: You’re in elite territory. Your existing customers are driving meaningful growth, reducing your dependence on new customer acquisition. This is where private equity firms start getting very interested.

Above 140%: You’re an outlier. Companies like Slack (before its acquisition), Datadog, and other platform plays that embed deeply into customer workflows can achieve these levels. At this stage, you’re essentially funded by your existing customer base.

These benchmarks come with an important caveat: they vary significantly by segment. Enterprise B2B SaaS companies often see higher NRR than SMB-focused products because enterprise customers have longer sales cycles but also more room to expand within large organizations. Product-led growth companies frequently outperform sales-led ones in NRR because they make it easy for users to upgrade as they discover more value.

The takeaway isn’t “you need 120%+ or you’re failing.” The takeaway is that NRR gives you a clear signal about whether your business model works. If it’s below 100% for more than a couple of quarters, something is fundamentally broken in your product-market fit or customer success operation.

Why NRR Is the Most Important SaaS Metric

Now for the controversial part: I’m going to argue that NRR matters more than ARR, MRR, CAC, LTV, or any other SaaS metric you might be tracking. Here’s why.

First, NRR measures the only thing that actually compounds. ARR is a vanity metric — it grows when you add new customers, but it tells you nothing about whether those customers will still be around next year. A company adding $5M in ARR with 70% NRR is actually declining in health despite the top-line growth. A company with $3M ARR and 140% NRR is arguably in better shape because its revenue is growing from within. When investors value SaaS companies, they increasingly apply multiples to revenue that will stick around, and NRR is the best proxy for stickiness.

Second, NRR connects directly to unit economics in ways other metrics don’t. Your Customer Acquisition Cost (CAC) only makes sense if customers stick around long enough to generate positive returns. But LTV calculations require assumptions about retention and expansion that NRR either validates or invalidates. If your NRR is 80%, your effective LTV is dramatically lower than if it’s 120%, regardless of what your spreadsheet assumptions say. The metric is a stress test for your entire business model.

Third, NRR predicts future revenue with more accuracy than any forecast. Your pipeline tells you what you might close. Your ARR tells you what you’ve already closed. But your NRR applied to your current customer base tells you what you’ll definitely have next period — because it’s based on existing relationships, not hypothetical ones. This is why sophisticated SaaS operators build financial models that project forward from current NRR rather than projecting from new logo targets.

Fourth, NRR is harder to game than other metrics. You can pump ARR with annual contracts and one-time fees. You can manipulate churn by defining it narrowly. But NRR captures the full arc of customer value — the good, the bad, and the ugly. It’s the most honest metric in your dashboard.

Here’s where I need to push back on conventional wisdom: NRR isn’t perfect, and treating it as the only metric that matters is a mistake. It can mask problems in specific customer segments. A company might show 120% NRR overall while SMB customers are churning at 40% annually — the expansion from enterprise customers hides the structural problem. It also ignores new customer acquisition entirely, which matters for early-stage companies still finding product-market fit. NRR is a metric for companies with an established base, not for startups validating their initial customer segment.

The right framework is this: NRR is your north-star metric for mature SaaS businesses, but it must be read alongside GRR (to understand baseline retention), CAC payback (to understand acquisition efficiency), and net new ARR (to understand total growth). No single metric tells the whole story, but NRR comes closest to a complete signal.

How to Improve Your Net Revenue Retention

Improving NRR requires addressing its components systematically. Here’s what actually works based on what high-performing SaaS companies do.

Invest in customer success with outcome-based programs. The companies with the highest NRR treat customer success as a revenue driver rather than a support function. This means assigning dedicated customer success managers to accounts, establishing clear success metrics for each customer segment, and creating systematic expansion triggers. When a customer reaches their success milestone, that’s when you introduce the next tier of value. Gainsight, the company that essentially invented the customer success category, reports that customers using their platform see NRR improvements of 15-25 percentage points on average.

Build expansion pathways directly into your product. Product-led growth works for NRR because it makes upgrading effortless. When users hit usage limits, show them the value they’d get from upgrading rather than just blocking their work. When they unlock a new feature, surface it prominently. Stripe’s dashboard shows customers exactly how much they’re saving by using more of the platform, making expansion feel like a natural next step rather than a sales push.

Create tiered pricing that rewards growth. Your pricing structure should align with how customers actually use your product. If power users are on the same plan as light users, you have no expansion pathway. HubSpot’s evolution from tiered pricing to usage-based elements as they added more products created multiple expansion vectors for their customer base. The key is ensuring that every pricing tier represents a genuine step up in value.

Reduce contraction by understanding why it happens. Contraction often precedes churn. When customers downgrade, that’s a signal — they’re telling you they were paying for value they weren’t using. Build systems to catch contraction early and understand the root cause. Sometimes the fix is as simple as helping them use features they’re paying for but haven’t discovered.

Address churn before it happens. Predictive analytics can identify customers at risk of churning before they cancel. Product usage drops, support ticket increases, and declining engagement scores are all leading indicators. Intercom and similar tools make it possible to create automated intervention sequences when these signals appear. The goal is churn prevention, not churn recovery — once a customer has decided to leave, it’s usually too late.

Focus on land and expand within organizations. If you’re selling to individual departments, you’re vulnerable to churn when that department’s budget changes or their champion leaves. The solution is expanding beyond the initial use case. Workday didn’t succeed by staying in HR software — they expanded into finance, analytics, and payroll. Each expansion creates a new root system that makes the customer relationship harder to dislodge.

Conclusion

Net Revenue Retention isn’t just another metric to track alongside dozens of others. It’s the metric that reveals whether your business model actually works — whether customers find enough value to stay and grow. ARR might get you board slides and press releases, but NRR determines whether your company will exist in its current form five years from now.

The SaaS industry is moving toward a world where capital is more expensive and investors are more discerning about quality over quantity. Companies with 140% NRR will continue to raise at premium valuations. Companies with sub-100% NRR will struggle to justify their growth narratives regardless of how fast their top line is growing.

The honest admission I’m willing to make: I don’t know what the “right” NRR benchmark is for every company. It depends on your segment, your growth stage, your pricing model, and your customer concentration. What I do know is that ignoring it — or treating it as just another vanity metric — is a choice that will cost you eventually.

If you’re not measuring NRR monthly, start now. If you’re measuring it but not acting on it, figure out what’s driving your expansion and contraction. If you’re already doing both, ask yourself whether you’re segmenting it enough to catch problems hiding in the averages.

The best SaaS companies don’t just acquire customers. They build relationships that become more valuable over time. NRR is how you know whether you’re actually doing that.