The startup funding landscape has changed a lot over the past decade. One of the biggest shifts: the pre-seed round has become its own distinct stage—something between having an idea and convincing traditional VCs to write a check. If you’re starting a company or thinking about investing at this earliest phase, understanding what pre-seed actually means—and who writes checks at this stage—can help you build momentum instead of stalling out before you truly begin.

Most founders assume they need a fully formed product before raising money. The reality is more nuanced. Pre-seed exists because experienced investors recognize that the earliest companies often need capital just to validate whether their core hypothesis holds water at all. This article covers what pre-seed funding actually is, who invests, how much you can raise, and what matters when you’re trying to close your first round.

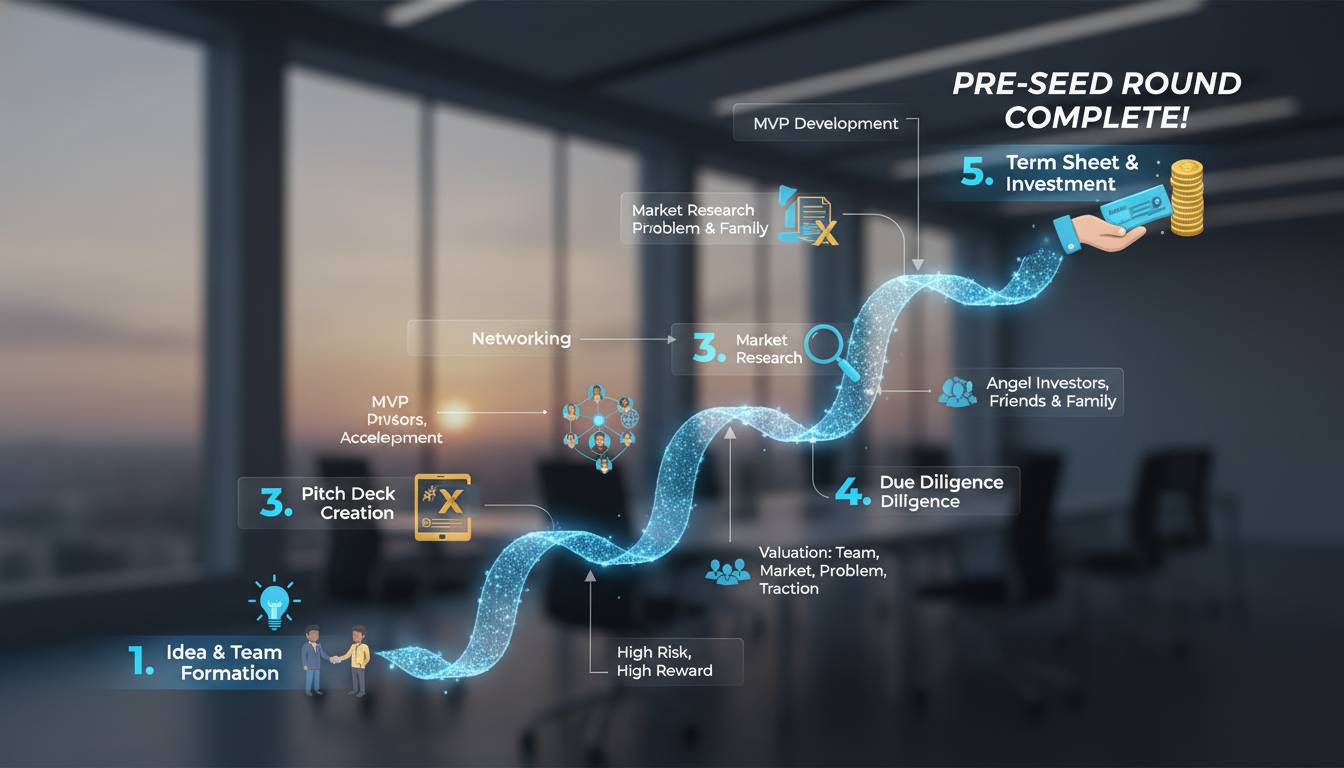

What Is a Pre-Seed Round?

A pre-seed round is the earliest formal equity financing a startup typically raises—usually before seed funding but after the company has moved beyond just an idea. The “pre” signals that this capital comes before the traditional seed stage. Companies at this point usually have a founding team, some early product work, and perhaps initial customer conversations, but they lack the traction metrics that seed-stage investors traditionally expect.

The stage became more prominent in the 2010s as venture capital became more accessible and accelerator programs proliferated. Before that, most early-stage funding jumped directly from friends and family into seed rounds. Now pre-seed has become its own category, with dedicated funds, syndicates, and even platforms designed specifically for this check size.

At pre-seed, you’re not building revenue at scale. You’re building proof of concept. You’re testing whether anyone actually wants what you’re selling, whether your team can execute, and whether the market opportunity is real enough to warrant further investment. The capital raised at this stage typically goes toward hiring your first engineers, designers, or salespeople; building a minimum viable product; or conducting customer discovery to validate your assumptions.

There’s no legal definition separating pre-seed from seed—the distinction is market convention. But in practice, pre-seed investments tend to happen when a company has more than an idea but less than the metrics (revenue, user growth, retention) that define a seed-stage company.

How Much Can You Raise at Pre-Seed?

Pre-seed rounds typically raise between $50,000 and $500,000, though the range varies significantly based on geography, industry, and the experience of the founding team. In major tech hubs like San Francisco, New York, or London, pre-seed rounds commonly land in the $250,000 to $500,000 range for strong teams. In secondary markets or for first-time founders working on capital-efficient businesses, $50,000 to $150,000 remains typical.

The valuations at pre-seed are notoriously difficult to pin down because they depend heavily on who is investing and how competitive the deal is. A first-time founder with no prior exits raising $100,000 might see a valuation somewhere between $1 million and $2 million. A repeat founder with a strong track record raising the same amount could command $3 million or $4 million. In hot markets or for particularly sought-after opportunities, pre-seed valuations have climbed even higher—some Y Combinator companies, for instance, have raised pre-seed rounds at valuations exceeding $5 million before Demo Day.

One important nuance: the amount you raise at pre-seed affects your options later. Raising too little leaves you underfunded and potentially unable to hit the milestones that seed investors want to see. Raising too much at too high a valuation can create challenges when you go to raise your seed round, especially if you haven’t made sufficient progress to justify the valuation bump. The sweet spot is raising enough capital to reach meaningful milestones—product launch, initial customers, clear traction—without over-optimizing for the headline number.

Who Invests at the Pre-Seed Stage?

The pre-seed investor ecosystem is diverse, ranging from individuals writing personal checks to specialized funds that focus exclusively on this stage. Understanding who these investors are—and what they’re looking for—helps you target the right sources of capital for your specific situation.

Angel Investors

Angel investors are high-net-worth individuals who invest their personal capital in startups, typically at the earliest stages. Many have experience as founders or executives themselves, which means they bring not just money but also mentorship, industry connections, and operational expertise.

Angels typically invest between $10,000 and $100,000 per company, though some “super angels” or angel syndicates write larger checks. They invest individually or as part of groups like AngelList syndicates, where a lead investor pools capital from multiple individuals to write bigger tickets. The Jason Calacanis-led LA Syndicate and the Sahil Lavingia-led Gumroad syndicate are examples of angel groups that have supported companies at pre-seed.

What angels look for varies widely, but most are betting heavily on the team—their ability to execute, their domain expertise, and their likelihood of being able to raise more capital later if the company succeeds. Many angels also invest defensively, taking small positions in many companies hoping that one becomes a breakout success. This is sometimes called the “spray and pray” approach, though more sophisticated angels are increasingly focused on writing larger checks into companies where they can add meaningful value.

Micro-VCs

Micro-VCs are venture capital firms that focus on writing smaller checks at earlier stages than traditional VCs. They typically manage funds in the $10 million to $50 million range and invest anywhere from $100,000 to $1 million at pre-seed and seed stages.

What distinguishes micro-VCs from angel investors is that they invest institutional capital—money from limited partners—so they have fiduciary obligations and fund lifecycles to consider. This means they’re often more process-driven than angels and may require more structured deal terms, board seats, or regular reporting.

Several micro-VCs have built strong reputations at the pre-seed stage. Precursor Ventures, for example, focuses almost exclusively on pre-seed, writing checks as small as $100,000 without requiring a lead investor. First Round Capital’s Dorm Room Fund specifically targets students and recent graduates. Hendo Ventures and Correlation Ventures are other examples of firms that have been active at this stage.

Micro-VCs often look for companies that have some early signal—early user waitlists, prototypes, or even informal letters of intent from potential customers—rather than just a pitch deck. They need to believe the company can become investable at seed, because their fund model depends on showing returns to limited partners within a 7-10 year window.

Accelerators

Accelerator programs have become a major source of pre-seed capital and mentorship. Programs like Y Combinator, Techstars, and 500 Startups provide funding in exchange for equity, along with intensive mentorship, structured curriculum, and access to networks of investors for follow-on funding.

Y Combinator, perhaps the most famous accelerator, currently invests $500,000 for 7% equity in every company in its batch—making it one of the larger pre-seed checks available. The program runs twice per year, and companies pitch to thousands of investors at Demo Day, creating enormous follow-on funding opportunities. But Y Combinator is extremely competitive; acceptance rates hover around 1-2%.

Techstars runs multiple programs globally, typically investing $120,000 for 6-7% equity. The structure varies by program—some are more industry-specific, while others are generalist. 500 Startups (now known simply as “500”) has invested in thousands of companies globally through its various accelerator and pre-seed programs.

Accelerators work best for founders who want structured support, community, and the credibility that comes with program acceptance. The tradeoff is giving up equity and committing to a program schedule that might not align with your company’s specific needs. Some founders skip accelerators entirely and raise directly from angels; others use accelerators as a launching pad, particularly if they’re first-time founders or entering a new market.

Friends and Family

Friends and family rounds remain one of the most common sources of earliest-stage capital, though they’re rarely called “pre-seed” in polite conversation. These investments typically come from people who know the founder personally and believe in them, rather than from professional investors evaluating the business on its merits.

The amounts vary widely—anywhere from a few thousand dollars to a few hundred thousand, depending on the wealth of the network. The terms are often less formal than professional rounds, sometimes structured as convertible notes that convert to equity at the next priced round, or simply as loans that convert to equity later.

There’s a practical reason to raise from friends and family before approaching professional investors: it demonstrates that people who know you best believe in what you’re building. It also gives you capital to build enough of a prototype or early traction to make your pitch to VCs more compelling. However, mixing personal relationships with investment carries risks. Everyone understands that most startups fail, but it’s different when the money belongs to your uncle or your college roommate. Clear communication about risk is essential.

Pre-Seed Funds

A growing category is the dedicated pre-seed fund—vehicles specifically designed to invest only at the pre-seed stage, writing checks from $50,000 to $500,000 and holding those investments through seed and Series A before exiting.

These funds have emerged because the gap between what angels can write and what VCs want to see has widened. As seed-stage checks have gotten larger (the median seed round in the US exceeded $4 million in 2023 according to PitchBook data), the pre-seed stage has become more formalized.

Examples of dedicated pre-seed funds include Wonder Ventures, Contrary Capital, and Day One Ventures, among others. Some corporate venture arms have also launched pre-seed programs, including Google for Startups and Salesforce Ventures.

Pre-seed funds typically have specific theses—some focus on specific geographies, industries, or founder profiles. Understanding their investment criteria helps you target the right funds rather than mass-emailing every pre-seed investor you can find.

What Do Pre-Seed Investors Look For?

The criteria at pre-seed differ significantly from later stages. At seed and Series A, investors look for metrics: revenue growth, user retention, cohort analysis, burning less than you’re earning. At pre-seed, there’s often no revenue to measure. Instead, investors evaluate different signals.

The team matters enormously. Who you are as founders—your background, your ability to recruit talent, your domain expertise, your resilience—is often the single most important factor. Investors at this stage are betting on people they believe can navigate the inevitable challenges of startup building. A strong team with a mediocre idea often beats a mediocre team with a strong idea at pre-seed.

The problem and market opportunity get careful scrutiny. Investors want to see that you’re solving a real problem for a meaningful number of people. They want evidence that you’ve talked to potential customers and that those conversations suggest demand. A compelling pitch deck shows customer interviews, waitlists, or letters of intent—not just projections of a $10 billion market.

Early traction, even if imperfect, helps. This might mean a waitlist with email signups, a prototype that a few people have tested, informal commitments from potential customers, or even just a compelling social media following that demonstrates demand. The key is showing that you’re not just hypothesizing—someone out there has expressed interest in what you’re building.

Your ability to raise more money is itself a signal. Investors at pre-seed know that most of their returns will come from companies that go on to raise seed and Series A rounds. If you can’t raise follow-on capital, their investment becomes worthless regardless of how promising the company seemed at pre-seed. Demonstrating that you understand the fundraising game and can articulate a credible path to your next round helps investors feel confident in backing you.

Pre-Seed vs Seed: What’s the Difference?

The line between pre-seed and seed has blurred considerably, but understanding the conventional distinction helps when planning your fundraising strategy.

Pre-seed rounds typically raise $50K-$500K, while seed rounds raise $500K-$4M+. Pre-seed valuations usually land between $1M-$5M, compared to $4M-$15M+ for seed. Pre-seed investors tend to be angels, micro-VCs, and accelerators, while seed rounds attract VCs, larger angels, and seed funds. The traction expected at pre-seed is just an idea, early prototype, or customer conversations—at seed, investors want an MVP, early users, and some revenue or strong growth metrics. The funds at pre-seed go toward building an MVP and validating your hypothesis, while seed funds scale the product, acquire customers, and build out the team.

The key distinction is that seed-stage investors expect to see you’ve moved beyond hypothesis testing into initial product-market validation. This might mean you have a working product, early paying customers, meaningful user growth, or some other evidence that the business model is viable. Pre-seed investors are more forgiving on metrics because they’re funding the work that generates those metrics.

Many companies raise pre-seed, then seed, then Series A—three distinct rounds. But some skip stages, raising a larger seed round that includes what would have been pre-seed capital. Others raise multiple pre-seed rounds, bringing in different investors as they hit milestones. The path isn’t linear, and the terminology is more convention than rule.

Recent Pre-Seed Round Examples

Looking at actual pre-seed deals helps ground the abstract definitions.

Y Combinator companies routinely raise pre-seed rounds both during and immediately after the program. In recent batches, companies like Moonshot, which built AI-powered educational tools, raised pre-seed rounds in the $500,000 to $1 million range. Many YC companies convert their YC funding into a larger pre-seed or seed round shortly after Demo Day.

Outside of accelerators, direct-to-consumer brands have raised pre-seed rounds from angel investors focused on consumer products. Companies in the AI space have seen particularly strong pre-seed activity, with investors eager to back founders building on the recent wave of foundation model capabilities.

In 2023 and into 2024, pre-seed activity moderated from the frenzied levels of 2021-2022, but companies with strong teams and compelling ideas continued to raise. The market has shifted toward greater scrutiny on fundamentals—investors want to see clearer paths to product-market fit before writing checks.

Conclusion

Pre-seed funding has become a legitimate, distinct stage in the startup fundraising journey—not just a consolation prize for companies that can’t yet raise seed. Understanding who invests at this stage, what they expect, and how much capital is available helps you approach fundraising strategically rather than desperately.

The most important takeaway is this: pre-seed investors are buying an option on your future success. They’re betting that you and your cofounders can figure out whether your idea has legs, build something people want, and ultimately raise enough capital to scale. Your job is to give them confidence that you understand the journey ahead and that you’re the team to navigate it.

What remains genuinely unresolved is whether the proliferation of pre-seed capital is ultimately good for founders. More options mean more companies can get started, but it also means more companies raise money before they’ve validated their ideas—potentially prolonging failure rather than forcing pivot or exit earlier. If you’re raising pre-seed, go in with eyes open about what you’re actually accomplishing with that capital. The check size is nice. The milestones you hit with it matter more.