Most people get VC wrong. They imagine steady returns — invest in ten startups, three fail, four break even, three return 2x, and you profit. That model works for private equity or hedge funds. Venture capital doesn’t work that way. Instead, returns follow the power law: a handful of investments generate returns that dwarf everything else combined. Everything else — most of your portfolio — is essentially noise.

This isn’t an opinion. It’s the defining characteristic of venture capital, and understanding it changes how you evaluate VC as an investor, a founder, or anyone allocating capital to startups. The power law isn’t something that happens occasionally. It is the fundamental structure of the entire asset class.

What the Power Law Actually Means for VC Returns

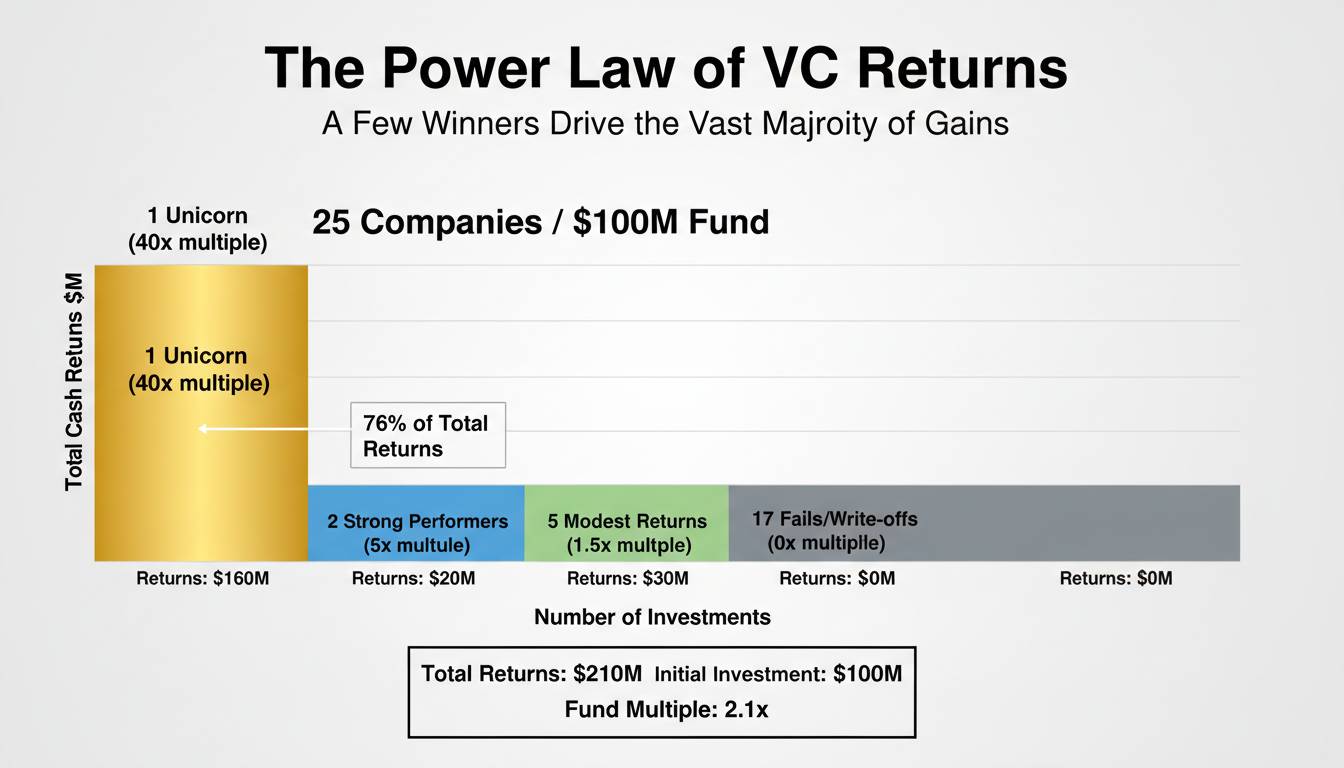

The power law describes a relationship where one variable changes in proportion to the other variable raised to some power. In plain English: a small number of things produce a disproportionately large share of the results. In venture capital, this means the top 1% or 2% of investments in a portfolio generate somewhere between 60% and 100% of total returns. The remaining investments might as well be losing lottery tickets.

If you invest $100 million across 100 companies, the math doesn’t split evenly. It concentrates. Your fund’s entire performance often rests on whether one or two investments become companies worth billions. Not millions — billions. A $50 million check that becomes a $10 billion company doesn’t just return your original capital. It returns 200x. No combination of modest successes replicates that.

Y Combinator, the well-known startup accelerator, has backed over 4,000 companies through 2024. But the returns concentrated in just a handful — Stripe, Dropbox, Airbnb, Reddit, Twitch — those four or five companies are worth more than the rest of the portfolio combined.

The Mathematics Are Worse Than You Think

Here’s where conventional wisdom gets it wrong. Many people assume a healthy VC portfolio has a “j-curve” — a few big winners, several modest successes, and some failures that cancel out. That might describe angel investing or early-stage accelerator portfolios. Institutional venture capital operates under far harsher math.

A 2019 study by Professors Andrew Metrick and Benjamin Yadlowsky at the University of Chicago found that the top 1% of VC investments by internal rate of return (IRR) produced returns roughly equal to the entire bottom 99%. The single best investment in a typical fund performs about as well as every other company in that fund combined.

This means that when a VC says they’re “looking for 10x returns,” they’re not describing a typical outcome. They’re describing the minimum threshold for the outlier that will actually move the fund’s performance. The other 90% of the portfolio can return 1x or 0x, and the fund’s ultimate result still depends almost entirely on whether those one or two bets hit.

Sequoia Capital’s early 1998 investment of $12.5 million in Google generated a return valued at over $10 billion at Google’s IPO in 2004. That’s roughly 1,000x. No reasonable portfolio modeling accounts for that kind of concentration. But it’s not an exception — it’s the rule.

Real Examples That Show How Extreme It Gets

Sequoia and Google get the most attention, but the pattern repeats across every successful fund.

Andreessen Horowitz’s bet on Facebook is a good example. Their $12.7 million investment in Facebook’s 2010 Series C valued the company at roughly $50 billion at IPO. By the time Facebook (now Meta) peaked in 2021, that stake was worth tens of billions. The fund’s other investments during that period — even successful ones like Airbnb, Lyft, and Slack — were rounding errors compared to the Facebook return.

Benchmark Capital’s 2004 investment of $5 million in Uber generated a return exceeding $7 billion. The same fund had other notable successes, but nothing came close. One investment produced returns that would have made the entire fund successful even if every other company had failed entirely.

Lowercase Capital, founded by Chris Sacca, provides another clear case. Their 2012 seed investment in Instagram sold to Facebook for $1 billion 18 months later — a return that probably exceeded 500x on paper before the acquisition. Again, one deal drove the fund’s reputation and returns.

The pattern is so consistent that top-tier VC firms have stopped pretending they can construct diversified portfolios in any traditional sense. They construct concentrated portfolios designed to maximize exposure to the outliers they hope to find.

Why Most VC Funds Cannot Beat Public Markets

This is where the power law becomes uncomfortable for the industry. Because returns concentrate in a few winners, most VC funds dramatically underperform public market indices over time.

Research from Fundfire and other analytics firms consistently shows that roughly two-thirds of VC funds never return more than the public market equivalent. The top quartile of funds generates returns that distort the entire industry’s average. If you’re a limited partner (LP) investing in a typical VC fund, the odds are against you.

This isn’t because VC managers are incompetent. It’s because the power law works both ways. Yes, a few funds capture enormous returns from their outliers. But the majority of funds — even well-managed ones with smart investors and good deal flow — simply cannot generate enough winners to overcome the math.

The implication is stark: most venture capital is not a good investment for most investors. The asset class only makes sense if you can access the top-tier funds — those with the deal flow, brand leverage, and network effects to actually win the outliers. Everyone else is paying high fees for below-market returns.

The Concentration Problem No One Talks About

Here’s the uncomfortable truth the industry rarely acknowledges: the power law means that even successful VC funds often underperform on a risk-adjusted basis.

Consider the math. A typical VC fund charges 2% management fees and takes 20% of profits (the “2 and 20” structure). Over a 10-year fund life, you’re paying roughly 20% of your returns to managers before they ever see a dollar of profit. To earn a 2x net return, you needed a gross return significantly higher.

Now add the power law’s concentration. Your fund’s entire outcome depends on one or two companies. If those companies succeed, you might get 4x or 5x net returns. If they fail — and startups fail at extraordinarily high rates — you get nothing. There’s no middle ground. The distribution of outcomes isn’t skewed. It’s binary.

This is why I think the conventional advice to “invest in venture capital for diversification” is seriously flawed for most people. You can’t diversify away the power law. You’re either in the concentrated winner-take-all distribution or you’re not. If you’re allocating a small percentage of a portfolio to VC, you’re not getting diversification — you’re getting a lottery ticket with terrible odds that will almost certainly expire worthless.

Common Questions About VC Returns

What percentage of VC investments actually return money?

About 40-50% of VC investments return less than 1x of invested capital. Roughly 25-30% lose money entirely. The remainder either return capital plus a small profit or generate meaningful returns. The key point is that even in successful funds, the majority of investments don’t produce notable returns.

Why do VC returns follow a power law?

Because startup outcomes follow a power law. The nature of building a company that attacks a massive market and captures majority share creates winner-take-all dynamics. Technology businesses exhibit strong network effects, economies of scale, and regulatory moats that accrue to the dominant player. There’s rarely a profitable #2.

How many companies does a VC fund need to invest in to get an outlier?

There’s no magic number. Top-performing funds might invest in 20-30 companies and get one or two outliers. Some funds invest in 100+ companies and still rely on a single winner. The key is getting into the outlier when it emerges, which requires deal flow that includes the best companies and the ability to write large enough checks to matter.

Do all VC firms follow the power law?

Yes, though the degree varies by stage. Early-stage funds (seed and Series A) typically see more extreme distributions because more companies fail. Later-stage funds see somewhat less extreme distributions because companies have already survived the initial risk period. But no VC strategy escapes the fundamental dynamics.

Why Understanding the Power Law Matters

If you’re evaluating whether to invest in a VC fund, the power law should inform every decision. First, only consider funds with genuine access to top-tier deal flow — the firms that can actually get into the companies most likely to become outliers. Second, understand that the fund’s entire performance will likely depend on whether one or two investments work. Third, recognize that most VC funds underperform public markets, and the median return is worse than you think.

If you’re a founder raising venture capital, the power law explains why investors behave the way they do. They’re not looking for safe bets. They’re looking for massive outcomes. Your pitch should acknowledge that reality and demonstrate how your company could become one of those outliers — because that’s the only thing that matters to them.

The power law isn’t going away. It’s the fundamental economics of startup investing, and anyone telling you otherwise hasn’t done the math. The question isn’t whether you accept it. The question is how you build a strategy that accounts for it.