The Rule of 40 is one of those metrics that sounds simple but tells you almost everything about how a SaaS company creates value. I first encountered it in 2015 while working with a growth-stage startup that had impressive top-line numbers but was burning cash at an alarming rate. The founders were convinced they were winning. Then a seed investor ran the Rule of 40 calculation, and suddenly the conversation shifted from “how fast can you grow” to “why are you choosing to lose money this aggressively?” That single number—growth rate plus profit margin—told a more complete story than any dashboard I’d seen.

Since then, the Rule of 40 has become a cornerstone of SaaS investing logic, championed by Andreessen Horowitz, Benchmark, and nearly every serious venture firm evaluating B2B software businesses. But here’s what most explainers get wrong: the rule is a guideline, not a law. It applies differently depending on company stage, market conditions, and competitive dynamics. Understanding when to use it—and when to ignore it—matters more than memorizing the formula.

The Rule of 40 Formula Explained

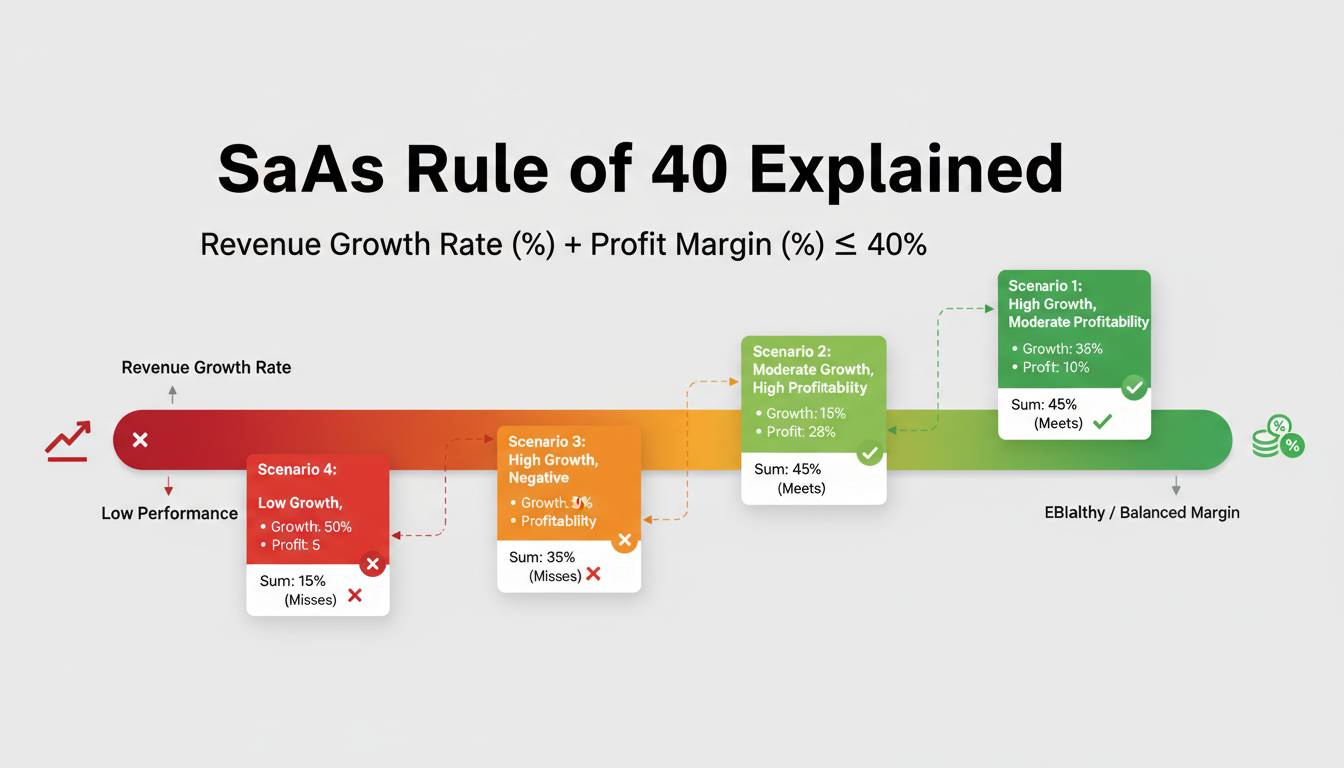

The Rule of 40 says a healthy SaaS company should have a combined growth rate and profit margin of at least 40%. That’s the whole thing:

Growth Rate + Profit Margin = 40%

Growth rate is usually measured as year-over-year revenue growth (sometimes quarter-over-quarter for faster-moving companies). Profit margin is your operating margin, though some investors use EBITDA margin or net margin depending on how they’re analyzing the business. Just be consistent—pick one and stick with it for comparisons.

A company growing at 60% year-over-year but losing 30% on operations scores a 30 on the Rule of 40. That’s a problem. A company growing at 15% but generating 35% operating margins also scores a 30—and that’s also a problem, just for different reasons. The first company is burning investor cash to buy growth that may not be sustainable. The second company has likely hit a ceiling and stopped investing in its future.

Conversely, a company growing at 25% with 20% operating margins scores 45—that’s healthy. So does a company growing at 50% and breaking even. The magic number is 40, and there are multiple ways to get there.

What Is a Good Rule of 40 Score?

Not every company needs to hit 40 at all times. Here’s how to think about it:

Above 40: Excellent. The company is growing fast while generating meaningful profit. This is the ideal state that most public SaaS companies aspire to reach. Companies like Atlassian have sustained scores above 40 for years by combining strong growth with expanding margins.

30-40: Good but imbalanced. A company in this range is doing something right. If they’re at 35 with 40% growth and -5% margins, they’re investing aggressively in growth—that’s a reasonable choice for a company still capturing market share. If they’re at 35 with 10% growth and 25% margins, they’re probably mature and might need to reinvigorate their growth engine.

Below 30: Concerning, unless there’s a clear explanation. This typically means either the company is burning too much cash to chase growth that isn’t materializing, or they’ve stopped investing in growth entirely and are harvesting the business. Neither is ideal for most investors.

The key insight is that the Rule of 40 isn’t a pass/fail test—it’s a diagnostic tool. A score of 25 might be perfectly acceptable for a two-year-old startup still finding product-market fit. It’s unacceptable for a company that’s been operating for a decade.

Examples of Companies That Pass the Rule of 40

Here are real examples because numbers without context are useless.

Salesforce has historically hovered around the Rule of 40 threshold. In their FY2024 results, they showed solid revenue growth paired with improving operating margins—the combination pushed them comfortably past 40 in most quarters. They’ve transitioned from hypergrowth mode to a more balanced profile as they’ve matured.

HubSpot is a consistently strong performer on this metric. The company has managed to maintain 20%+ revenue growth while expanding margins into the mid-teens, giving them Rule of 40 scores well above 40 for several consecutive years.

Snowflake presents an interesting case. They’ve shown remarkable revenue growth—often exceeding 100% year-over-year—but their margin profile has been negative as they invest heavily in go-to-market and product development. Their Rule of 40 score has been below 30 despite the impressive top-line growth. This is exactly the scenario where the metric reveals tension between growth investment and profitability.

Atlassian deserves special mention because they’ve been one of the rare companies to sustain Rule of 40 scores above 50 for extended periods. Their cloud-first model with high gross margins and efficient go-to-market has allowed them to grow at 30%+ while generating 25%+ operating margins. That’s exceptional.

The pattern here is clear: companies that pass the Rule of 40 consistently share certain characteristics. High gross margins (typically 75%+), efficient customer acquisition costs, and the ability to scale revenue without linear cost increases. If you’re evaluating a SaaS company and they can’t explain why their score is below 40, that’s a red flag worth investigating.

When Growth Matters More Than Profit

Here’s where I want to push back on the conventional wisdom. The Rule of 40 was developed primarily for evaluating late-stage private companies and public SaaS businesses. It doesn’t apply cleanly to early-stage startups, and applying it indiscriminately will lead you to make poor investment decisions.

If you’re looking at a Series A company doing $2 million in ARR, demanding they hit a 40 on the Rule of 40 is absurd. They’re still finding product-market fit. They’re still hiring their first engineers. The entire point of early-stage investing is that you’re sacrificing profitability for the chance at outsized growth. A company at $2M ARR that’s profitable is probably not taking enough risk.

The Rule of 40 becomes relevant once a company has found repeatable go-to-market motion. That typically means $10M+ in ARR, 100%+ year-over-year growth, and some evidence that they can scale without burning through cash at an accelerating rate. Before that point, you should be looking at different metrics: customer acquisition cost payback period, net revenue retention, and product-market fit indicators.

There’s also the question of market timing. In 2021, capital was abundant and cheap. Investors were willing to accept Rule of 40 scores in the 20s if growth was accelerating. Companies were prioritized for their growth trajectory, with the assumption that profitability would come later. Then interest rates rose, public market multiples compressed, and suddenly the Rule of 40 mattered again. Companies that had optimized purely for growth found themselves in difficult positions.

The lesson: the Rule of 40 is a useful lens, but it’s not the only lens. Context matters enormously. A company in a rapidly expanding market with strong competitive positioning can justify below-40 scores for longer than a company in a commoditizing market with weak differentiation.

Limitations of the Rule of 40

I’ve already hinted at some limitations, but let me be explicit because this is where most explainers fail to give you the full picture.

It doesn’t account for capital efficiency. Two companies can both score 35 on the Rule of 40, but one might be generating that through efficient operations while the other is burning through venture capital. The metric treats a dollar of profit the same as a dollar of investor cash spent on growth. That’s a meaningful distinction.

It can incentivize short-term thinking. If a company is sitting at a 42 and growing 15% with 27% margins, they might choose to harvest the business rather than invest in new initiatives that would lower their score temporarily. This is particularly relevant for public companies facing quarterly earnings pressure.

It misses quality of growth. Not all revenue growth is equal. A company growing 50% through land-and-expand within existing accounts is in a different position than one growing 50% through discounting. The Rule of 40 treats these identically, which can be misleading.

It doesn’t factor in capital structure. A company with zero debt and $100M in the bank can afford to run lower margins than one with covenant-heavy debt obligations. The Rule of 40 is blind to balance sheet strength.

It assumes growth and profit are interchangeable. In reality, some markets reward growth more than others. A company competing in a winner-take-all market might be right to sacrifice profitability for market share. The Rule of 40 doesn’t capture that strategic choice.

The metric works best when you’re comparing similar companies at similar stages in similar markets. Apply it broadly without those qualifiers, and you’ll draw incorrect conclusions.

How to Calculate Your SaaS Company’s Rule of 40

Let me walk you through the calculation step by step, because there’s more nuance than just adding two numbers together.

Step 1: Determine your growth rate. Take your revenue from this fiscal year and divide by revenue from the prior fiscal year. Subtract 1 and multiply by 100 to get a percentage. If you have $15M this year and $10M last year, your growth rate is 50%.

For private companies that don’t report publicly, you’ll typically use year-over-year ARR growth. Some investors prefer last-twelve-month (LTM) revenue to smooth out seasonality.

Step 2: Determine your profit margin. Operating margin is the most common choice—operating income divided by revenue. You can also use EBITDA margin if you want to exclude the effects of depreciation and amortization. For companies still heavily investing in R&D, some investors look at contribution margin (revenue minus cost of goods sold and variable sales costs).

Let’s say your operating income is $3M on $15M in revenue. That’s a 20% operating margin.

Step 3: Add them together. Growth rate (50%) + Operating margin (20%) = 70%. That’s an excellent score.

Here’s a practical example with real numbers:

| Company | Revenue (FY) | Prior Year Revenue | Growth Rate | Operating Income | Operating Margin | Rule of 40 Score |

|---|---|---|---|---|---|---|

| SaaS Co A | $50M | $35M | 43% | ($5M) | -10% | 33 |

| SaaS Co B | $50M | $40M | 25% | $10M | 20% | 45 |

| SaaS Co C | $50M | $25M | 100% | $0 | 0% | 100 |

Company A is growing fast but burning money—they’re at 33, which is borderline. Company B has found balance at 45. Company C is growing extraordinarily fast and breaking even—at 100, they’re maxing out the scale, though they might want to start generating profit at some point.

Calculate this quarterly and track the trend. A company that’s declining from 45 to 35 to 28 over three years is signaling a problem, even if they’re still technically above 40.

Frequently Asked Questions

Is the Rule of 40 still relevant in 2025?

Yes, perhaps more than ever. The funding environment has shifted dramatically since the easy-money days of 2020-2021. Investors are now more skeptical of growth-at-all-costs strategies and are demanding a demonstrated path to profitability. The Rule of 40 provides a simple framework for evaluating whether a company is striking that balance. If anything, the metric has become more important, not less.

What is the ideal Rule of 40 for a public SaaS company?

For public companies, investors generally expect scores above 40 as a baseline. Companies consistently below 40 face pressure from analysts and may see their stock multiples compress. That said, some highly valued public SaaS companies have traded at premiums despite lower scores if they’re growing very fast. As of early 2025, the market is still rewarding growth, but the tolerance for unprofitable growth has decreased.

Should early-stage startups worry about the Rule of 40?

No. If you’re investing in a startup with less than $5M in ARR, the Rule of 40 is the wrong metric. Focus on whether they have product-market fit, whether customers are renewing and expanding, and whether they have a credible path to repeatable sales. You’ll know it’s time to apply the Rule of 40 when the company starts talking about scaling efficiently.

Can a company have a Rule of 40 above 100?

Technically yes, if you add growth rate and profit margin. A company growing 120% with -10% operating margins would score 110. But there’s no magic threshold at 100—the Rule of 40 is a minimum threshold for health, not a ceiling for excellence. Companies with scores significantly above 40 are typically either extremely fast-growing, extremely profitable, or both.

Conclusion

The Rule of 40 endures because it does something few SaaS metrics accomplish: it forces you to look at two critical dimensions of business health simultaneously. Growth without profitability is a mirage. Profitability without growth is an epitaph. The companies that build lasting value find ways to balance both, and the Rule of 40 helps you identify whether they’re succeeding.

But here’s the honest admission this article needs: no single metric tells the whole story. The Rule of 40 is a filter, not a decision. It helps you quickly eliminate companies that are clearly unhealthy and focus your due diligence on those that pass the threshold. From there, you still need to understand revenue quality, customer retention, competitive positioning, and a dozen other factors that no single number can capture.

The companies that will thrive in the coming years are those that treat the Rule of 40 as a constraint to work within, not a score to maximize. Growth is optional. Profit is optional. Sustainable value creation requires both—and that’s the harder problem the metric was always meant to illuminate.