Most founders get this wrong: they assume angel investors and venture capital firms are essentially the same thing—just different sizes of the same funding pool. That’s a dangerous oversimplification that can cost you both money and control of your company. The differences between angels and VCs aren’t just about check size. They’re about fundamentally different incentive structures, risk tolerances, and what you’re actually signing away when you take the money.

I’ve watched founders chase VC funding when they would have been better served by an angel, and vice versa. The choice isn’t about how much capital you need—it’s about what kind of partner you want running alongside you for the next decade. Let me explain what actually separates these two worlds, because the conventional wisdom on this topic is looser than the people writing about it want to admit.

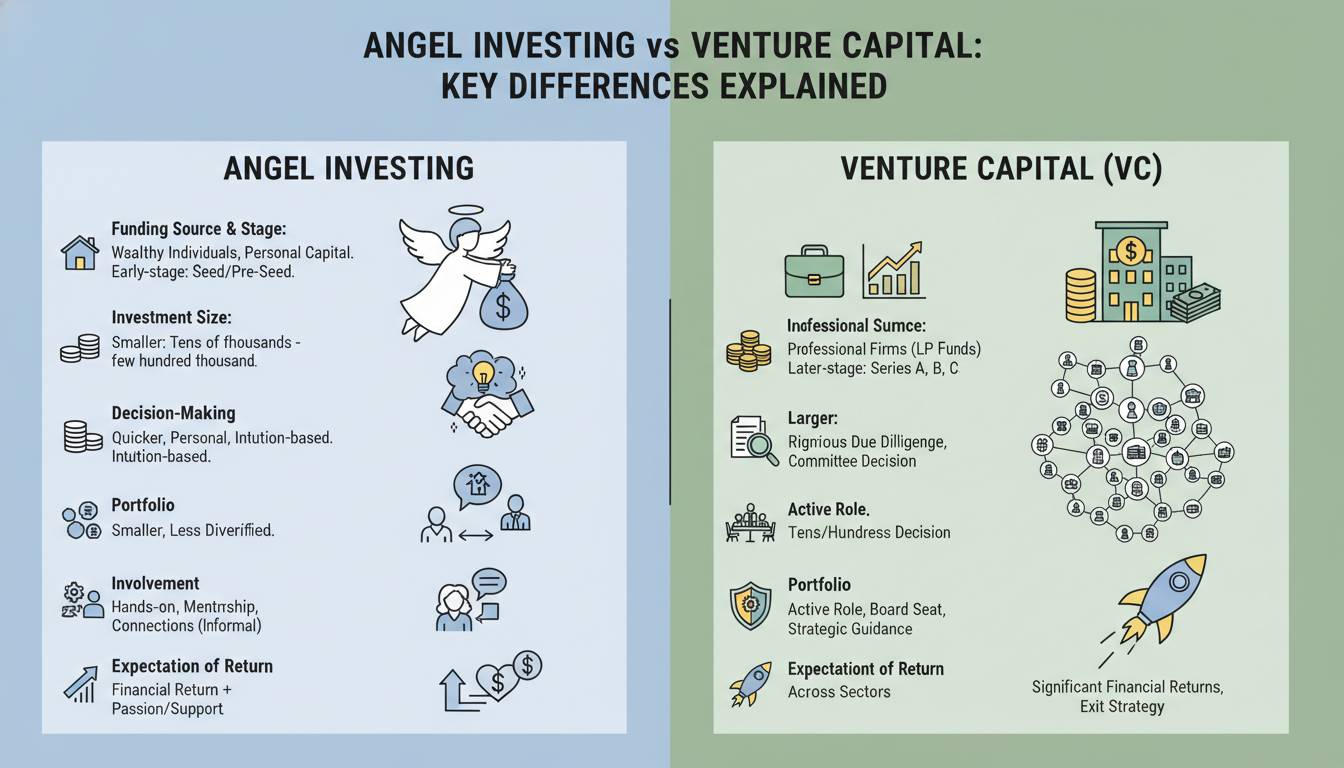

What Angel Investors Actually Are

Angel investors are individual wealthy people who put their own money into startups—typically at the earliest stages, often before a company has any revenue or even a full product. They’re not funds. There’s no institutional LP structure. It’s someone’s personal capital, and they get to decide individually how to deploy it.

The name comes from the early days of startups when wealthy individuals would provide capital to entrepreneurs in exchange for equity, essentially “angelic” compared to the harsh terms from banks or predatory lenders. That framing has stuck, but the reality is more complicated. These aren’t charity cases. Angels are sophisticated investors who expect significant returns; they just operate on different timelines and with different resources than institutional funds.

Most angels invest anywhere from $10,000 to $250,000 in a given company, though some “super angels” or angel syndicates can write larger checks. They’re often the first external capital a startup raises—commonly called pre-seed or seed funding—and they typically invest after friends and family rounds but before venture capital firms would consider the deal.

The key characteristic that separates angels from institutional money is that they’re investing personal wealth. This changes everything about how they evaluate deals, how long they can wait for returns, and what kind of operational help they’re capable of providing. When an angel writes you a check, they’re not just investing in your company—they’re betting their own money in a way that a fund manager, who earns fees regardless of outcome, simply cannot replicate.

What Venture Capital Actually Is

Venture capital firms manage pooled capital from institutional investors—pension funds, endowments, family offices, and wealthy individuals—who commit money to a fund that will be invested across dozens of startups over typically a 10-year period. The VC firm takes a management fee (usually 2% of assets under management annually) and takes a share of any profits (typically 20%, called “carried interest” or “carry”).

This structure matters enormously. A VC firm has fiduciary obligations to its LPs. They can’t write checks based purely on intuition or founder relationships the way an angel might. They need to build portfolios, manage risk across multiple investments, and show their LPs a coherent investment thesis. This institutional layer fundamentally changes how they operate.

VC firms almost always invest at later stages than angels—Series A and beyond, though some firms now write seed checks. Their checks are substantially larger, typically starting at $1 million and going up from there into the tens or hundreds of millions for later-stage rounds. A company raising a $15 million Series B is almost certainly dealing with VCs, not angels.

The other critical difference is that VC firms have dedicated teams. You might meet one or two partners during the fundraising process, but once you’re in their portfolio, you gain access to the firm’s full network of other founders, service providers, and follow-on capital. Angels can certainly help with introductions, but they can’t match the institutional infrastructure that a VC firm brings to bear on your problems.

Investment Amounts: The Numbers That Actually Matter

The conventional comparison is lazy. People say “angels invest less, VCs invest more,” which is true but uselessly vague. What actually matters is the range and the implications of those ranges.

Early-stage angels typically write checks between $10,000 and $100,000. “Super angels” or angel groups might go to $250,000 or occasionally $500,000, but that’s rare and usually involves multiple angels pooling money. The average angel check across all investments in the US is somewhere in the $25,000 to $50,000 range, though averages obscure enormous variation.

VC firms, even at seed stage, typically want to write minimum checks of $500,000 to $1 million to justify the overhead of due diligence and portfolio management. Series A rounds commonly raise $3 million to $15 million. By Series B and beyond, you’re looking at $20 million to $100 million+ rounds. These aren’t just bigger numbers—they represent fundamentally different company stages and capital needs.

The practical implication is this: if you need $50,000 to build your MVP and prove initial traction, chasing VC funding is a waste of time. The deal flow is too competitive, the check sizes are too large relative to your needs, and the expectations around governance and reporting would overwhelm your current capacity. Conversely, if you’ve built a product that’s generating $500,000 in ARR and you need $5 million to scale, an angel probably can’t help you—their individual check sizes are too small to move the needle at that stage.

There’s a legitimate middle ground where founders need somewhere between $200,000 and $1 million. This is arguably the hardest money to raise, because it’s too much for most individual angels but too little to attract serious VC attention. Many companies at this stage turn to angel syndicates, accelerator programs, or smaller VC funds that focus specifically on this “seed” range.

Funding Stages: When Each Investor Enters

The funding stage conversation is where I see the most confusion among first-time founders. People hear “seed round” and assume it’s VC money, but that’s often wrong. Many seed rounds are primarily angel-funded, and some “pre-seed” rounds have VCs writing checks alongside angels.

Pre-seed is almost exclusively angel territory—sometimes called “family, friends, and fools,” though that framing is increasingly outdated. This is the earliest possible stage, where you’re building your first product, testing initial hypotheses, and often haven’t generated any revenue. Angels take the highest risk here, which is why they demand the highest equity percentages.

Seed is the gray area. You have some evidence of product-market fit—maybe early users, maybe initial revenue, maybe strong engagement metrics—but you’re not yet ready for the full scaling play that VCs want to see. Both angels and VCs invest at this stage, though the VC firms that do seed deals are typically either specialized early-stage funds or are writing small checks as part of a relationship-building strategy for later, larger rounds.

Series A and beyond is where VCs dominate. At this point, you have measurable traction—revenue, user growth, retention data—and you’re looking for substantial capital to scale the business model that’s proven itself. The investment amounts are too large for individual angels, and the due diligence requirements match institutional capabilities.

One thing the articles don’t tell you: stage definitions are collapsing. In 2024-2025, the line between seed and Series A has blurred considerably. Some VCs now invest “seed” checks that would have been considered Series A five years ago. The amounts matter less than what the investor expects in terms of traction and what they’re willing to pay for it.

Equity and Ownership: What You’re Giving Away

This is where founders consistently get burned—not because the math is complicated, but because they don’t understand what different investors optimize for.

Angels typically take equity in the range of 5% to 20% for their earliest checks, depending on valuation, the competitive dynamics of the deal, and how far along the company is. A $25,000 check at a $2 million pre-money valuation represents 1.25% equity. The same check at a $500,000 pre-money valuation is 5%. Angels at these early stages are taking significant risk, so they need meaningful ownership to make the math work on the upside.

VCs, because they’re investing larger amounts at later stages, typically take smaller percentages—but the dollar value is vastly larger. A $5 million Series A at a $20 million pre-money valuation represents 20% ownership. That’s the same percentage as a tiny angel check, but the VC now owns $4 million worth of value (at post-money) versus the angel’s portion being worth almost nothing until there’s an exit.

The more important question than percentage is control. VCs almost always demand board seats, protective provisions (veto rights over major decisions like raising additional capital, selling the company, or making large expenditures), and information rights that are far more extensive than what angels typically require. An angel might ask for a board observer seat or regular updates. A VC will require formal board representation and quarterly financial reporting with covenants you’ll need to comply with.

Here’s something most articles won’t tell you: sometimes giving up more equity to an angel at an earlier stage can actually be better for your long-term outcome than taking less equity from a VC at a later stage. That’s because the control provisions matter more than the headline percentage. A VC who owns 15% but controls your board can force decisions you disagree with. An angel who owns 10% but has no board power cannot.

Level of Involvement: What Support Actually Looks Like

The myth of angel involvement is that angels provide hands-on mentorship, strategic guidance, and their full network to help you succeed. The reality is more uneven. Some angels are incredibly active and helpful. Others write a check and disappear for years.

Active angels—typically successful entrepreneurs themselves—can be extraordinary resources. They can help you hire, think through strategic decisions, introduce you to potential customers or later-stage investors, and serve as a sounding board for difficult problems. The best angels have been where you’re going and remember what it was like.

VC firms, by contrast, are institutional. They have portfolio teams that coordinate support across companies. They’ll connect you with other founders in their portfolio who have faced similar challenges. They have dedicated platform teams that help with recruiting, communications, and go-to-market strategy. This is infrastructure that individual angels simply cannot match.

But, the quality of VC involvement varies enormously by firm and even by partner within a firm. Some VC partners are incredibly hands-on, spending real time with their portfolio companies. Others are “check writers” who primarily add value at the board level and during fundraising moments. You don’t always get to choose which type you’re working with.

My honest assessment: for most first-time founders, the operational support matters less than people think. What matters more is whether the investor is someone you trust, someone who will be honest with you when things are going poorly, and someone who won’t panic when you hit rough patches. Both angels and VCs can provide that. Neither guarantees it.

Risk and Return Profiles: The Economics That Drive Everything

The structural differences between angels and VCs create completely different risk-return calculations, and understanding this is essential for choosing which path to pursue.

Angel investments are high-risk, high-potential-return, but the economics are personal. An angel who invests $50,000 in ten companies needs just one of those ten to return 10x or more to make money overall. With individual checks being small relative to their overall net worth, angels can afford to swing for the fences. They’re not managing a portfolio with LP obligations—they’re making personal bets.

VCs have different math. Their LPs expect them to return capital within a fund lifecycle (typically 10 years), and the industry benchmark is that the top handful of investments in a portfolio drive essentially all the returns. But because VC funds are managed professionally, there’s more pressure to show consistent performance and to avoid catastrophic losses. The institutional structure creates pressure toward different risk profiles.

The return expectations differ too. Angels, investing at the earliest stages, are looking for 10x, 20x, or even 100x returns on their winners to compensate for the high failure rate. VCs, investing later at higher valuations, typically target 3x to 5x returns on their money—still excellent by traditional standards, but reflecting the lower risk profile of later-stage investing.

One thing that surprised me when I first learned about this industry: the absolute returns for individual angels can sometimes exceed what VC funds generate, even though VC funds manage vastly more capital. An angel who puts $25,000 into a company that gets acquired for $50 million (a 2000x return) has made more money personally than many VC partners see from their funds. This is why some wealthy individuals prefer angel investing despite the higher risk, because the asymmetric upside potential is so much greater.

Which is Right for Your Startup?

This is the question every founder needs to answer honestly, and the answer depends on factors that have nothing to do with how much money you need.

Choose angel funding if: You’re in the earliest stages with minimal traction. You want to maintain maximum control over decisions. You’d prefer to move fast and iterate rather than build toward a massive scaling play. You’re comfortable with a longer timeline to exit (or no exit at all). Your network and mentorship needs can be met by one or two experienced individuals.

Choose venture capital if: You’ve already proven some form of product-market fit. You need substantial capital to scale a business model that’s already working. You’re building toward a large outcome (hundreds of millions or billions in value). You want access to institutional infrastructure and follow-on capital. You’re comfortable giving up board control and accepting the governance requirements that come with institutional money.

The reality is that many successful companies have used both. They started with angel money to prove initial concepts, then raised VC funding to scale after demonstrating traction. The path isn’t either/or, it’s often sequential.

What I wish more founders understood is that the choice also reflects what kind of company you want to build. Angel-funded companies can stay small, profitable, and founder-controlled for years or decades. VC-backed companies are implicitly on a path toward acquisition or IPO, because that’s how VC funds return money to their LPs. There’s no right answer here, but you need to be honest with yourself about which trajectory you’re signing up for.

Frequently Asked Questions

What’s the main difference between angel investors and VCs?

The core difference is that angels invest their own personal money while VCs manage pooled institutional capital. This creates different incentive structures, risk tolerances, and levels of operational involvement. Angels can move faster and take bigger risks on unproven concepts. VCs have governance requirements and portfolio-level considerations that shape how they invest and support companies.

How much do angel investors typically invest compared to VCs?

Individual angels typically invest $10,000 to $100,000 in early-stage companies, while VC firms usually write checks starting at $1 million for seed rounds and significantly larger amounts for Series A and beyond. Some angel groups can coordinate larger investments, but the scale difference remains substantial.

Do angel investors take more equity than VCs?

Not necessarily. Both angels and VCs take equity proportional to the investment amount and company stage. Angels investing at pre-seed or seed stages often take higher percentages (5-20%) because the risk is greater. VCs investing at Series A and later typically take smaller percentages but own substantial dollar value. The control provisions that come with VC equity often matter more than the percentage itself.

Which is better for early-stage startups, angel or VC?

For companies in the earliest stages with minimal traction, angel funding is typically the better choice. VCs at those stages are competitive to access and may impose governance requirements that overwhelm a nascent company. Once you’ve demonstrated product-market fit and need substantial capital to scale, venture capital becomes the more appropriate path.

The funding landscape continues shifting. Angels have become more organized through syndicates and platforms like AngelList. VC firms have moved earlier in company lifecycles, creating more competition for deals that used to be exclusively angel territory. The line between the two worlds is blurrier than ever, and the best founders learn to navigate both depending on what their company needs at each stage.

What remains constant is the fundamental truth that choosing your investors is choosing your partner for the hardest parts of building a company. The money matters less than the relationship. Figure out what you actually need—not just financially, but strategically and operationally—and find the investor whose incentives align with where you want to take the business.