The first time a founder hears their company is valued less than the previous round, it’s a gut punch. Yet down rounds happen more often than the startup ecosystem prefers to admit. Understanding what a down round actually signals—not just for the company’s financials, but for its culture, trajectory, and competitive position—matters far more than the headline valuation number itself.

A down round isn’t simply a funding failure. It’s a recalibration, sometimes necessary and sometimes avoidable, that reveals uncomfortable truths about how a startup is performing against the market’s expectations. The way founders, employees, and investors respond to this moment often determines whether the company survives or becomes another cautionary tale.

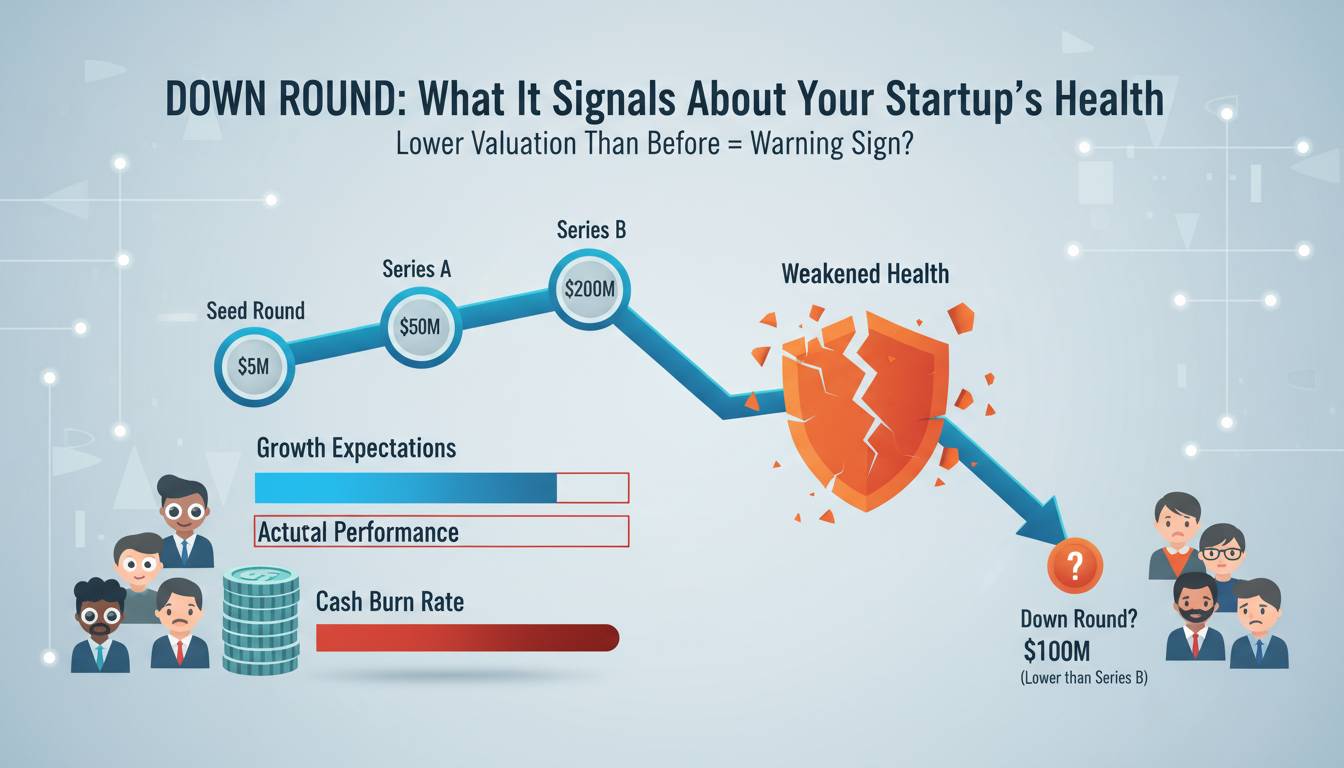

This article covers what down rounds actually mean, why they happen, what they signal about your startup’s health, and how to navigate them.

A down round occurs when a company raises capital at a lower valuation than the valuation assigned in its previous funding round. If your Series A valued the company at $50 million and your Series B raises capital at a $40 million pre-money valuation, you’ve executed a down round.

The mechanics are straightforward: existing shareholders, including founders, early employees, and prior investors, own a smaller percentage of the company after the round closes. New capital comes in, but the price per share is lower than what previous investors paid. This isn’t just accounting—it represents a fundamental shift in how the market values your business.

Distinguishing between a true down round and other financing events matters. A flat round, where valuation stays approximately the same, isn’t technically a down round, though employees often experience it similarly since option grants may not appreciate. An up round is the opposite: new money values the company higher than previous investors did. The direction of your round tells a story about whether your company is gaining or losing ground in the market’s eyes.

Why Do Startups Experience Down Rounds?

The causes fall into several buckets, and understanding which one applies to your situation matters enormously.

Market conditions represent the most common culprit. When public markets correct or venture capital activity slows, as happened dramatically in 2022 and persisted into early 2023, investors become dramatically more conservative. Companies that raised at peak valuations in 2021 found themselves facing completely different funding environments by 2022. This isn’t a failure of execution; it’s a change in the discount rate the market applies to private companies.

Performance misses are harder to escape. If your revenue growth fell short of projections, if your product-market fit cratered, or if key milestones didn’t materialize, investors will price that risk into a new round. The gap between expectation and reality gets reflected in a lower valuation. Founders need to be honest about whether they’re facing a market correction or an execution problem, or both simultaneously.

Runway concerns create a dangerous dynamic. When a company burns through cash faster than projected and has twelve months or less of runway, it loses negotiating leverage dramatically. Investors know you’re desperate, and they’ll price that into their terms. This is where bridge rounds and extensions often become down rounds—the company needs capital to survive, and the only way to get it is to accept worse terms.

Down rights and anti-dilution provisions sometimes force down rounds mechanically. Some investor contracts include provisions that trigger if subsequent financing happens at lower valuations, either by converting preferred stock to common or by issuing additional shares to prior investors. These provisions can compound the dilution beyond what the headline valuation suggests.

One counterintuitive reality: sometimes a down round is the smartest move a founder can make. If the alternative is running out of cash and shutting down, accepting a lower valuation to stay alive preserves optionality. We’ll explore recovery later, but this point matters because the startup press tends to treat down rounds as existential failures, when sometimes they’re actually rational survival decisions.

What Does a Down Round Signal About Startup Health?

Here’s where founders and employees need to hear an uncomfortable truth: a down round is a signal, not a diagnosis. It tells you something about how the market views your company, but it doesn’t automatically determine your fate.

Reality check on expectations. The most important signal is that your previous valuation was probably too high relative to your actual performance. Markets are efficient over time, and a down round is a correction. The question to ask is whether the previous valuation was a genuine market assessment or whether it was inflated by hype, FOMO, or favorable market conditions that have since changed.

Weakened negotiating position. Future fundraising will be harder. New investors will point to the down round as evidence of risk, and existing investors may have preferences or restrictions that complicate the process. Your ownership stake is smaller, which affects incentive structures for everyone.

Potential talent implications. This is the signal many founders underestimate. When a company raises at a lower valuation, the implied value of employee stock options decreases. Top performers who have other options may leave. This creates a retention challenge that compounds the company’s problems.

Strategic inflection point. A down round often forces clarity. Companies that were trying to do too many things must focus. Ambiguity about product-market fit gets resolved—you either have it or you don’t. This can be valuable even though it feels painful.

The honest acknowledgment most articles skip: down rounds are sometimes signaling mechanisms for problems that existed long before the funding event. A company with genuine product-market fit and strong unit economics can usually raise money without a down round, even in difficult markets. If you’re experiencing a down round, the probability that something fundamental needs fixing is high, not because markets are unfair, but because markets are actually pretty good at detecting underlying business quality over time.

Notable Down Round Examples

Real examples illustrate how varied down round outcomes can be.

Snapchat’s parent company Snap went public in 2017 and saw its public market valuation drop significantly below private valuations at various points. While not a private down round, the dynamic shows how market sentiment can reverse dramatically. Snap navigated this by focusing on advertising revenue growth and eventually stabilized its position.

Zenefits represents a more dramatic case. The HR software company saw its valuation plummet from $4.5 billion to around $2 billion in a 2016 down round driven by regulatory issues and management upheaval. The company eventually recovered under new leadership, but the journey took years and required fundamental restructuring.

WeWork’s 2019 crisis led to a valuation collapse from $47 billion to around $8 billion when the IPO failed and SoftBank took control. This wasn’t a traditional down round, it was a near-death experience that required extreme intervention. The company has since gone public again at much lower valuations, demonstrating that even catastrophic collapses can sometimes lead to eventual stabilization.

What separates companies that recover from those that don’t? Usually three factors: whether the underlying business still has genuine value, whether leadership can make hard decisions quickly, and whether enough capital exists to execute a turnaround. Not every down round company has these elements.

What a Down Round Means for Employees

If you’re an employee at a startup facing a down round, the implications hit your finances directly.

Option pool dilution means your existing grants represent a smaller percentage of the company. If you have 100,000 options that were worth $1 each at a $50 million valuation, they’re worth less when the company is valued at $40 million, even though nothing changed about your actual grant. The strike price of new options you receive will be lower, which is technically advantageous, but the total value of your equity package has decreased.

Vesting and acceleration. Some employment agreements include change-of-control provisions that accelerate vesting if the company is sold for less than certain thresholds. Review your offer letter and equity agreement carefully. You may have protection you don’t know about, or you may discover you’re more exposed than expected.

Retention grants. Companies facing down rounds often issue new option grants to existing employees to offset the dilution. These grants typically have lower strike prices, making them more valuable in a recovery scenario. However, companies in distress may not have enough authorized shares to issue meaningful grants.

The decision to stay or leave. This is personal and depends on your confidence in the company’s recovery, your financial situation, and your other options. Don’t make the decision based on company announcements alone. Talk to people who know the business deeply, assess the runway honestly, and consider whether you believe in the current leadership’s ability to execute a turnaround.

One thing worth noting: employees often overreact to down rounds in the short term. A down round doesn’t mean the company is going to zero tomorrow. Many companies continue operating for years after a down round, and some eventually recover and go public or get acquired at higher valuations. Your decision should be based on an honest assessment, not panic.

Can a Startup Recover from a Down Round?

Yes, startups can recover from down rounds. The path is harder, but it’s been navigated successfully.

Focus on fundamentals. After a down round, companies often need to cut costs dramatically, narrow their product focus, and extend runway. This can be painful but it’s often necessary. The companies that recover tend to emerge leaner and more focused than before.

Demonstrate traction. The best signaling mechanism after a down round is revenue growth or user growth that exceeds expectations. If you can show investors metrics that outperform the conservative assumptions built into your down round valuation, you create a foundation for an up round.

Consider strategic alternatives. Sometimes the best path isn’t another venture round. Acquihires, strategic acquisitions, or even controlled shutdowns with asset sales can deliver better outcomes than years of struggling to raise the next round. Not every company needs to go public, and not every company should try to.

Time heals some wounds. A down round from 2022 looks different in 2024 if the company has stabilized and grown. Markets forget, and a company that looked like a failure two years ago might look like a bargain today if metrics have improved.

The honest limitation here: recovery isn’t equally likely for everyone. If your market is shrinking, your competitive position is weakening, or your technology is becoming obsolete, no amount of cost-cutting will save you. Down rounds don’t create these problems, they reveal them. The recovery question isn’t really about the down round; it’s about whether the underlying business has a viable future.

How to Navigate a Down Round

For founders facing this reality, the path forward requires clear thinking.

Control the narrative internally. Your team will be anxious. Be honest about the situation, explain what it means and doesn’t mean, and outline your plan. Uncertainty is more damaging than bad news delivered clearly.

Explore all financing options first. Before accepting a down round, consider venture debt, revenue-based financing, strategic investments, or even customer advances. Anything that can extend runway without diluting valuation may be worth pursuing.

Negotiate terms carefully. If a down round is inevitable, pay attention to liquidation preferences, anti-dilution provisions, and board composition. A slightly higher valuation with aggressive terms can be worse than a lower valuation with founder-friendly terms.

Focus on runway. Calculate exactly how long your cash lasts under various scenarios. Assume fundraising will take longer than expected. Plan for the worst case.

Protect your option pool. Fight to maintain enough authorized shares for employee retention grants. Your people are your only asset after a down round, don’t lose them because you can’t issue equity.

For employees: ask questions. How much runway does the company have? What’s the plan for the next fundraising round? Are there retention grants in the works? Don’t accept vague answers. You need to make decisions with accurate information.

For investors: this is where your reputation matters. Leading a down round with appropriate terms, providing follow-on capital if you can, and treating founders fairly builds the kind of relationships that generate returns over a career. The investors who nickel-and-dime founders during vulnerable moments tend to get deal flow that reflects their values.

Conclusion

A down round isn’t the end of your startup journey, it’s a turn in the road. It signals that the market has recalibrated its expectations for your company, and that recalibration contains information you shouldn’t ignore.

The companies that recover treat down rounds as forcing functions for clarity. They cut what isn’t working, focus on what is, and build from a more honest foundation. The companies that don’t recover tend to spend energy avoiding the implications of what the down round revealed.

What matters most isn’t the valuation number itself, it’s what you do with the time and capital you have left. A down round can be the crisis that forces necessary change, or it can be the beginning of a slow decline. The difference usually comes down to honest assessment, decisive action, and the ability to focus on fundamentals rather than optics.

If you’re facing a down round right now, the pressure is real. But the question isn’t whether you’ve failed, it’s whether you have the clarity and courage to build something valuable from here.