If you’re raising venture capital for the first time, the term sheet will likely land on your desk before anything else from an investor. It’s not the final document—far from it—but it determines the fundamental economics and control dynamics of your company for years to come. What many founders don’t realize is that term sheets are almost entirely negotiable, and the difference between a good term sheet and a predatory one often comes down to understanding what each clause actually means for your equity, your decision-making power, and your eventual exit. This guide breaks down every term you need to know, why it matters, and where you should push back.

What Is a Term Sheet and Why Should You Care?

A term sheet is a non-binding agreement that outlines the basic terms and conditions under which an investment will be made. Think of it as the blueprint before the building begins—it establishes the key economic terms (valuation, investment amount, equity percentage), governance rights (board seats, voting), and protections (liquidation preferences, anti-dilution) that will eventually be drafted into binding legal documents like the Stock Purchase Agreement and Investor Rights Agreement.

The “non-binding” part is crucial. Most term sheets contain language stating that neither party is obligated to complete the transaction until definitive agreements are signed. However, the term sheet does create certain obligations—typically around exclusivity, meaning you agree not to shop the deal to other investors for a specified period (usually 30 to 60 days).

What surprises many first-time founders is how much variance exists between term sheets from different investors. A $5 million term sheet from one investor can look radically different from another $5 million term sheet in terms of your actual ownership, control, and future flexibility. Understanding these differences isn’t just helpful—it’s essential for negotiating from a position of knowledge rather than trust.

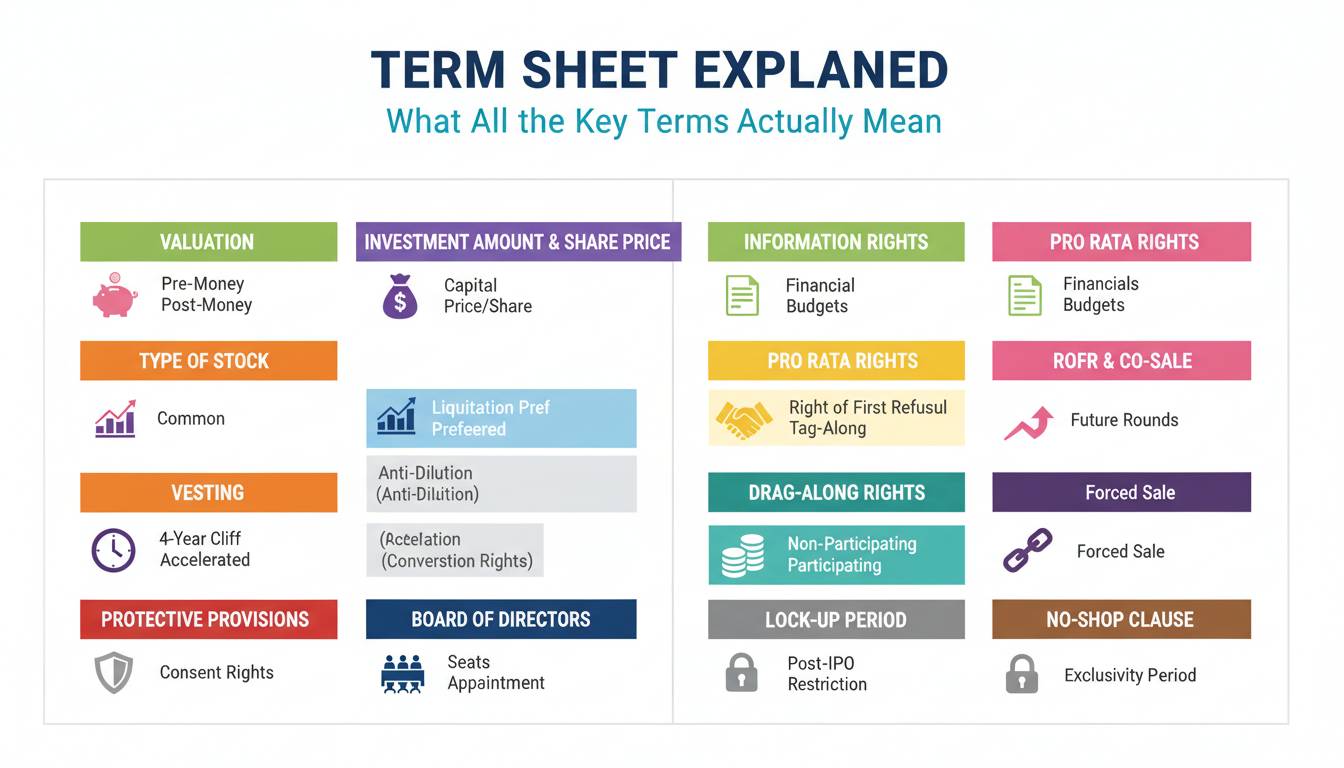

Key Terms in a Term Sheet: The Complete Breakdown

Every term sheet revolves around several core categories: economics and valuation, ownership and control, investor protections, and exit mechanisms. Below is a detailed breakdown of each term you’re likely to encounter, with explanations of what they mean in practice rather than in legal abstraction.

Valuation: The Foundation of Your Deal

Pre-Money vs. Post-Money Valuation represents the most visible number in any term sheet, but the distinction between these two figures directly impacts your ownership percentage. Pre-money valuation is what the company is worth before the new investment comes in; post-money valuation equals pre-money plus the investment amount. If a investor offers $2 million on a $8 million pre-money valuation, they own 20% of the company post-money ($2M ÷ $10M). The same $2 million investment on a $10 million pre-money valuation gives the investor only 16.7% ownership. Many founders focus exclusively on the pre-money number, but the math matters just as much.

Option Pool is often the most misunderstood term on a term sheet. The option pool represents shares reserved for future employee grants, typically ranging from 10% to 20% of total shares. Here’s the catch: the option pool is usually created before the new investment closes, which means it dilutes your existing shares. If a term sheet creates a 15% option pool on a pre-money basis, that 15% comes out of your existing equity before the investor’s money enters the picture. This is one of the most common areas where investors can structure deals to their advantage—founders should always ask whether the option pool is pre-money or post-money and push for post-money if possible.

Economics and Ownership

Liquidation Preference determines what happens when your company is sold or liquidated. In a “1x non-participating” liquidation preference (the standard in most venture deals), investors get their money back first, and then they convert to common stock and share pro-rata with other shareholders. In a “participating” preferred stock structure, investors get their money back AND keep their ownership percentage in the remaining proceeds. A 2x liquidation preference means investors get twice their investment before anything goes to common shareholders. For founders, this is a critical term—favorable exits can be dramatically reduced by aggressive liquidation preferences.

Anti-Dilution Provisions protect investors if the company raises money at a lower valuation in the future (a “down round”). The most common is “weighted average” anti-dilution, which adjusts the conversion price based on how much money was raised and at what price. “Full ratchet” anti-dilution is far more punitive—it simply adjusts the investor’s conversion price to match the new lower price, effectively giving them more shares. Most venture deals use weighted average, but founders should be wary of full ratchet provisions as they can massively dilute common shareholders in down-round scenarios.

Control and Governance

Board Composition defines who sits on your company’s board and in what proportions. A typical structure for a company with institutional investors gives investors two seats, founders two seats, and an independent seat agreed upon by both parties. The key question for founders is whether you maintain board control. If you have two investor seats and two founder seats with no independent, you effectively share control. Many founders make the mistake of accepting investor-majority boards without recognizing what that means for their operational autonomy.

Voting Rights specify how investors can vote on company matters. Most preferred stock votes alongside common stock on an as-converted basis, meaning each preferred share gets a vote equal to the number of common shares it can convert into. However, certain decisions may require the approval of a majority or supermajority of preferred stockholders voting as a separate class—these “class voting” provisions can give investors blocking power over major corporate actions.

Investor Rights and Protections

Pro-Rata Rights (also called preemptive rights) allow existing investors to participate in future funding rounds to maintain their ownership percentage. If you raise a new round and an existing investor has pro-rata rights, they can invest enough to keep their percentage whole. The practical effect is that pro-rata rights can make it harder for new investors to enter a deal, because existing investors can effectively block them by exercising their rights. Some investors waive pro-rata in writing, while others insist on maintaining them.

Information Rights require the company to provide regular financial reports to investors—typically quarterly unaudited statements and annual audited statements. These rights are standard and usually terminate upon IPO when the company becomes publicly reporting.

Protective Provisions (sometimes called “veto rights” or “negative covenants”) require investor approval for certain major actions, regardless of board composition. These typically include: issuing new equity above certain thresholds, selling or merging the company, incurring debt above a specified amount, changing the board size, or amending the certificate of incorporation. Founders should pay close attention to which actions require investor approval and the thresholds involved—a protective provision requiring investor consent to raise any round over $500,000 effectively gives investors control over your fundraising timeline.

Conversion and Exit

Conversion Rights allow preferred stock to be converted into common stock at any time, at the election of the holder. Most term sheets include automatic conversion provisions—preferred stock converts to common upon a qualified IPO (typically $50 million+ in proceeds and minimum price per share) or upon a vote of the majority of preferred stockholders. The conversion ratio starts at 1:1 but can be adjusted by anti-dilution provisions.

Redemption Rights give investors the ability to force the company to buy back their shares if certain conditions aren’t met—typically if the company hasn’t gone public or been acquired within a certain timeframe (often 5 to 7 years). While redemption rights are included in many term sheets, they rarely get exercised in practice, and their inclusion doesn’t necessarily mean you’ll face a forced buyback. However, the existence of redemption rights on the cap table can complicate future fundraising, as new investors may view them as a liability.

Drag-Along Rights allow a majority of shareholders (or the board) to force minority shareholders to sell their shares in the event of an acquisition. This prevents a minority holder from blocking a deal that the majority wants to close. Tag-Along Rights work in the opposite direction—if a major shareholder sells their stake, smaller shareholders have the right to sell their proportional amount on the same terms. These provisions protect both sides in exit scenarios.

Common Mistakes Founders Make With Term Sheets

The biggest mistake is treating the term sheet as a take-it-or-leave-it document. Investors expect negotiation—it’s standard practice, and accepting the first version without pushback signals naivety rather than professionalism. A second common error is focusing exclusively on valuation while ignoring governance terms. A company valued at $10 million with founder-friendly governance is often better long-term than a $12 million deal with investor-majority board control and full ratchet anti-dilution.

Another pitfall is not understanding what’s “market” for your stage and sector. Seed deals typically have different term norms than Series A, and consumer SaaS companies face different expectations than biotech startups. Research what comparable companies in your sector have accepted, and use that as your baseline for negotiation rather than assuming every term should be founder-friendly.

Term Sheet vs. Letter of Intent: What’s the Difference?

The terms “term sheet” and “letter of intent” (LOI) are sometimes used interchangeably, but they serve different purposes depending on context. In M&A transactions, an LOI typically covers both economic terms and some binding provisions like exclusivity and confidentiality. In venture financing, the term sheet is usually the document that precedes the LOI.

The practical distinction: a term sheet is typically shorter (5-10 pages) and explicitly non-binding except for exclusivity and confidentiality. An LOI can be more detailed and may include binding terms on things like employee retention or earnouts. For venture financing, you’ll almost always deal with a term sheet rather than an LOI.

Frequently Asked Questions

Is a term sheet legally binding?

The term sheet itself is almost always non-binding—it’s a framework document. However, two specific provisions are typically binding: confidentiality (the investor won’t disclose what they’ve learned) and exclusivity (you won’t solicit other offers during the specified period). Everything else can be walked away from without legal consequences, though breaking exclusivity improperly can trigger issues.

How long is a term sheet valid?

Term sheets typically include an expiration date, often 30 to 60 days from issuance. This gives both parties time to complete due diligence and negotiate definitive documents. If the deal isn’t finalized before expiration, the investor can withdraw the offer—or simply let it lapse.

Can you negotiate term sheet terms?

Every term on a term sheet is negotiable. Some terms are more negotiable than others—valuation and board composition tend to be harder to move, while specific protective provisions and option pool size often have more flexibility. The key is understanding what matters most to you and what matters most to the investor, then trading where you have flexibility.

What happens after a term sheet is signed?

Once both parties sign the term sheet (indicating agreement to the key terms), the company enters an exclusivity period. The investor conducts detailed due diligence—reviewing financials, contracts, intellectual property, and legal matters. Simultaneously, lawyers draft the binding agreements based on the term sheet. If due diligence reveals no deal-breakers and the documents are finalized, the investment closes.

Moving Forward With Confidence

Term sheets don’t have to be intimidating documents that you sign because you feel you have no other option. The founders who negotiate the best deals are the ones who understand what each clause means for their company’s trajectory, who know which terms are market-standard and which represent overreach, and who approach the negotiation as a business discussion rather than a favor being granted.

Your equity is the most valuable asset you’ll create in your company’s early years. Understanding what a term sheet actually contains—and what those terms mean in practice—isn’t optional knowledge for a founder. It’s the foundation of every fundraising negotiation you’ll ever have.