Most investors jump straight to revenue growth when evaluating a tech company. They see 100% year-over-year growth and assume they’re looking at a winner. Then they get blindsided six months later when the company announces it’s out of cash. The missing piece is almost always burn rate — the metric that tells you how fast a company is consuming its cash reserves, and arguably the most important number for assessing whether a tech investment will survive long enough to deliver returns.

Burn rate isn’t just an accounting metric. It’s a window into a company’s discipline, runway, and ultimately whether management can execute without running out of money. Understanding it separates investors who get seduced by flashy growth from those who can actually assess survival risk. I’ve spent over a decade analyzing SaaS companies for institutional investors, and I can tell you that some of the most impressive growth stories of the last decade collapsed precisely because their burn rate was never sustainable. WeWork looked like a revolution in workspace. Theranos looked like the future of blood testing. In both cases, the underlying economics were burning cash at rates that could never be financed indefinitely.

This article gives you a framework for evaluating burn rate in any tech company. You’ll learn exactly how to calculate it, what numbers actually matter, how to interpret runway, and most importantly, how to spot the red flags that should make you walk away from an investment — no matter how compelling the growth story sounds.

Burn rate represents the total amount of cash a company spends each month minus any cash it generates from operations. It’s typically expressed as a monthly figure, though you can annualize it for certain analyses. The simplest way to think about it: if a company burned $2 million last month, that’s how much less cash it has in the bank than it started with.

Tech companies, particularly SaaS businesses and growth-stage startups, burn cash for a specific reason that distinguishes them from traditional businesses. They invest heavily in product development, sales, and customer acquisition with the expectation that each customer will generate far more revenue over their lifetime than it costs to acquire them. This unit economics model — often called the lifetime value to customer acquisition cost ratio, or LTV:CAC — creates an inherent timing mismatch. The cash outflow happens now. The cash inflow happens later. Until the business reaches scale where customer revenue exceeds acquisition and service costs, it must burn cash to fund that growth.

This is fundamentally different from a traditional company, which might burn cash during a downturn but generally generates positive operating cash flow. A healthy tech company in its growth phase can show impressive revenue while simultaneously burning millions monthly. That’s not necessarily a problem — it depends entirely on whether the burn is purchasing future growth at reasonable prices, or whether it’s simply purchasing survival.

The distinction matters because burn rate tells you how long the company can continue operating under its current trajectory. A company burning $500,000 monthly with $6 million in the bank has twelve months of runway. That same company burning $3 million monthly has only two months. Same revenue growth trajectory, completely different risk profile.

Gross Burn Rate vs. Net Burn Rate: The Critical Distinction

Most people discussing burn rate don’t distinguish between these two numbers, and that confusion leads to terrible investment decisions. Here’s the difference.

Gross burn rate is simply total monthly operating expenses. It includes salaries, rent, software subscriptions, marketing spend, everything the company spends money on to keep the lights on and the product moving forward. If you added up every line item on the company’s income statement, that’s your gross burn.

Net burn rate is what remains after subtracting any revenue the company generates. This is the number that actually matters for runway calculations. A company with $3 million in monthly expenses but generating $1 million in monthly revenue has a net burn of $2 million — not $3 million.

The distinction matters because it reveals whether the business model has any underlying economics at all. A company with $10 million in gross burn but $9.5 million in revenue is burning only $500,000 monthly. A company with $5 million in gross burn but zero revenue is burning $5 million monthly. The first company might be approaching profitability. The second company is completely dependent on external financing to survive.

When you’re analyzing a company’s SEC filings or pitch deck, always calculate net burn yourself. Many companies will happily highlight their gross burn as if it represents their cash consumption, when in reality their revenue is masking a much smaller net burn. Conversely, some companies in the early stages have zero revenue by design — they should be judged on their gross burn, because there’s no revenue yet to net against.

For SaaS companies specifically, pay attention to the gap between gross burn and net burn over time. If that gap is widening — meaning revenue is growing faster than expenses — the company is approaching sustainability. If that gap is narrowing or staying flat while revenue grows, something is wrong with the business model. Growth is getting more expensive, not less.

How to Calculate Burn Rate From Financial Statements

The formula is straightforward: take your ending cash balance, subtract the starting cash balance from a prior period, and divide by the number of months in that period. That’s your average monthly net burn.

But there’s nuance in the calculation that separates sophisticated analysts from beginners. Here’s how to do it right.

First, look at the cash flow statement in the company’s 10-Q or 10-K filing. Find the “cash used in operating activities” line. This tells you how much cash the company consumed to run its business before accounting for investing and financing activities. This is your operating cash burn.

However, this number can be noisy. Large one-time payments or seasonal fluctuations can distort a single month’s burn. The standard practice is to calculate a rolling average over the last three to six months to smooth out volatility. If a company spent $10 million in January due to a major marketing campaign but only $3 million in February, you don’t want to use either number in isolation.

For private companies that don’t file with the SEC, you’ll typically get burn rate information from the pitch deck or directly from management. Look for monthly cash consumption figures over the trailing twelve months. Ask specifically about the most recent month — management will often present averages that hide a deteriorating trend in the most recent data.

Let me walk through a real example. Suppose a company reports the following monthly cash flows over six months: negative $1.2M, negative $1.1M, negative $1.3M, negative $1.0M, negative $1.4M, negative $2.0M. The six-month average is about $1.33 million monthly. But the trend is clear: burn accelerated significantly in month six. Using only the six-month average would miss this deterioration. Calculate both the average and look at the trend.

Another important consideration: distinguish between “normal” operating burn and one-time expenses. If a company spent $5 million on a lawsuit settlement in a single quarter, that’s not reflective of ongoing cash consumption. Adjust for these items to get a clean picture of sustainable burn.

What Is a Good Burn Rate? The Answer Nobody Wants to Hear

Here’s where I need to push back on conventional wisdom, because every article on this topic will give you a percentage or ratio and tell you it’s the benchmark. They’re wrong, or at least incomplete.

There is no universal “good” burn rate. A company burning $5 million monthly with $100 million in the bank is in better shape than one burning $500,000 monthly with $3 million in the bank. The relationship between burn rate and cash on hand matters far more than the absolute number.

What matters is whether the burn rate is sustainable given the company’s stage and market position. An early-stage company with product-market fit and a clear path to profitability should be judged differently than a growth-stage company still searching for its business model. A public company with consistent revenue should be approaching positive cash flow or have a clear, credible plan to get there.

Here’s a framework that works better than arbitrary benchmarks:

Seed-stage companies (pre-revenue): Expect high burn relative to cash raised. The question isn’t whether they’re burning cash — it’s whether they’re burning it on things that will de-risk the business. Product development, founding team, early customer validation. Burn on anything else is a red flag.

Series A through C companies (early growth): By this stage, you should see evidence of improving unit economics. Customer acquisition costs should be declining or at least stable. Gross margins should be expanding. Burn should be purchasing growth at prices that make sense. If CAC is rising while the company raises more capital, that’s a warning sign.

Growth-stage and public companies: Burn should be declining as a percentage of revenue, or the company should be generating positive operating cash flow. If a company is doing $100 million in annual revenue and still burning $50 million annually, there needs to be an exceptional explanation — massive new market expansion, a transformative acquisition, something that justifies continued cash consumption.

The honest answer is that burn rate can be justified at almost any level if the return on that capital investment is sufficiently high. The real question isn’t whether burn is high or low — it’s whether the company is generating commensurate value from that investment.

Runway: The Number That Actually Matters

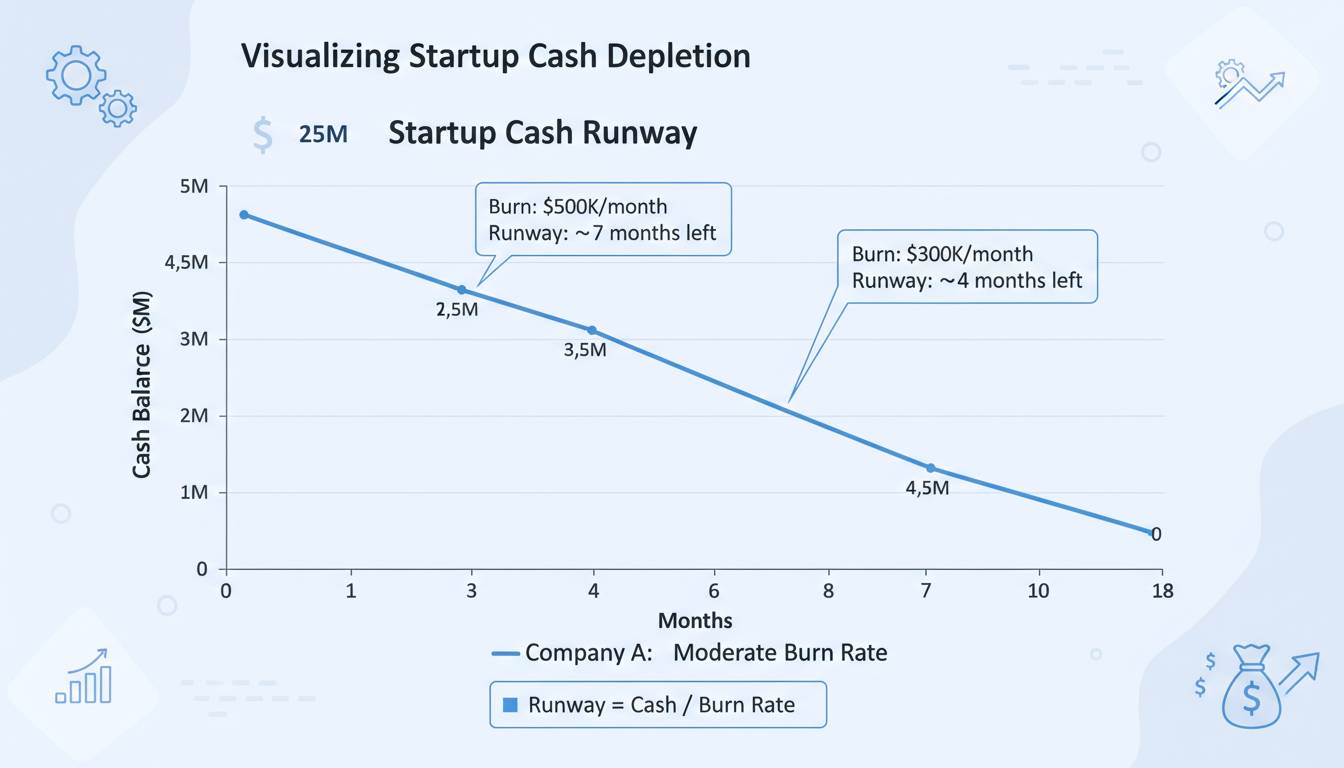

Burn rate is just an input. The number you should actually focus on is runway — how many months of operation the company can sustain with its current cash balance and burn rate.

The calculation is simple: divide cash on hand by monthly net burn. A company with $24 million in the bank burning $2 million monthly has twelve months of runway. But there’s a critical nuance that most investors miss: runway assumes burn rate stays constant. It almost never does.

Companies typically burn more cash as they grow. They hire more people, open more offices, spend more on marketing. So runway calculated today is usually optimistic. The more sophisticated approach is to project burn rate forward based on the company’s growth plans and see how runway evolves under different scenarios.

When analyzing runway, consider these factors:

Planned capital raises: If the company expects to raise more capital, their runway might extend beyond what current cash suggests. But this introduces risk — future fundraising depends on market conditions, investor sentiment, and company performance. Don’t count on a funding round that hasn’t closed.

Milestone dependency: Some companies have runway that extends to a specific date when they expect to hit a major milestone — product launch, FDA approval, contract signing. If that milestone slips, runway shortens. Ask what happens if key milestones are delayed by three to six months.

Burn rate flexibility: Can the company quickly reduce burn if needed? A company with mostly fixed costs (salaries, rent) can’t easily cut burn in a crisis. A company with mostly variable costs (marketing, contractor spend) has more flexibility. This matters for evaluating true risk.

Here’s a practical example. Company A has $20 million in cash, burns $1 million monthly, and expects to raise a Series C in 18 months. On the surface, they have 20 months of runway. But if the fundraising market deteriorates and they can only raise at a lower valuation in 24 months, they need to survive an extra six months. Company B has the same $20 million but burns $800,000 monthly and has more variable costs they can cut. Company B has more cushion against uncertainty, even though Company A might have a more promising business.

Always calculate runway under pessimistic scenarios. What happens if revenue misses projections? What happens if the planned fundraising takes longer or doesn’t happen? These stress tests reveal the real risk.

Red Flags: When Burn Rate Signals Danger

After analyzing hundreds of tech investments, I’ve developed a mental checklist of burn rate red flags that have proven remarkably predictive of problems. These aren’t always deal-killers, but they warrant serious investigation.

Burn rate growth outpacing revenue growth. This is the most common warning sign. A company that’s doubling revenue while tripling its burn is not building a business — it’s building a cash incinerator. At some point, the music stops and there isn’t enough capital to keep the lights on. The ratio of burn growth to revenue growth should be declining over time, not increasing.

Acquisition costs that are rising instead of falling. The SaaS model depends on achieving scale efficiencies in customer acquisition. If your CAC is going up while your LTV is staying flat or declining, you’re in a deteriorating business. Ask for cohort data that shows whether customers acquired in different periods have different economics.

Gross margin compression. If the company is making less money on each unit of revenue over time, that’s a structural problem. Maybe hosting costs are rising. Maybe competitive pressure is forcing price cuts. Whatever the cause, declining gross margins mean burn rate will rise even if revenue stays flat.

Key person dependency. Many early-stage companies burn cash because they’re paying premium rates for limited talent. That’s sometimes necessary. But if the company’s survival depends on one person who could leave, that’s risk that doesn’t show up in the financial statements.

Board conflicts or management turnover. This one is harder to quantify, but I’ve seen it repeatedly: companies with burn rate problems often have management turmoil. Founders fighting with each other or with the board. Executives leaving. This is often a symptom of cash pressure rather than a cause, but it accelerates problems.

A cautionary example: WeWork’s S-1 filing in 2019 revealed the company was burning over $700 million annually while its revenue growth was decelerating. The valuation being sought — $47 billion — implied continued access to unlimited capital at favorable terms. When the IPO collapsed and SoftBank took over, the burn rate had made the company dependent on continued financing that no longer came. The business couldn’t survive on its own economics.

Another example closer to venture scale: countless consumer apps that raised massive Series A and B rounds based on impressive user growth, only to discover that their CAC was so high relative to eventual monetization that they would need to raise capital indefinitely. Many of these companies had to either shut down or sell at fire-sale prices when the funding market tightened.

Analyzing Burn Rate in SEC Filings: A Practical Guide

For public companies, the SEC filings contain more detailed information than most investors bother to read. Here’s where to look and what to find.

The 10-K (annual report) gives you the most comprehensive view. Look for the cash flow statement and find “cash used in operating activities.” Compare this to revenue to see the cash conversion cycle. A company that needs to burn $1.50 to generate $1.00 of revenue has worse economics than one that burns $0.50.

The 10-Q (quarterly reports) let you track trends. Has the burn rate been consistent, or is it accelerating? Are there one-time items that distort the picture? The MD&A (Management Discussion and Analysis) section often explains significant changes in cash consumption.

The S-1 or S-3 filing (for companies going public or issuing new securities) is particularly valuable because it contains forward-looking projections. The company will often disclose its expected burn rate and runway. This is information the company wants investors to see, so it’s typically reliable, but always sanity-check it against historical data.

For private companies, look for the data room or pitch deck that was used in the fundraising. The quality of financial projections tells you something about management discipline. Companies that project flat burn for three years while projecting hockey-stick revenue growth are usually wrong about at least one of those numbers.

One specific metric worth calculating: the burn multiple. This is net burn divided by net new ARR (annual recurring revenue). A burn multiple of 1.0 means the company is burning one dollar to generate one dollar of annual revenue. A burn multiple of 0.5 means it’s burning fifty cents to generate one dollar of revenue. Lower is better. As a general rule, SaaS companies should be targeting burn multiples below 1.0 and declining over time.

The Burn Rate Conversation That’s Missing From Most Investment Analysis

Here’s the counterintuitive point that most articles on this topic get wrong: burn rate matters less than what the company is burning cash on.

A company spending aggressively on sales and marketing while acquiring customers profitably is building a sustainable business, even if the headline burn number looks alarming. A company burning cash on overhead and executive salaries while its core business loses money on every customer is in trouble, even if its burn rate looks manageable.

The key question is always: what am I buying with this cash expenditure? Is the company investing in assets that will appreciate (customer relationships, proprietary technology, brand) or is it spending to stand still (overhead, compliance, management perks)?

I also want to acknowledge a genuine limitation of this analysis. Burn rate analysis works best for companies that are burning cash. Many profitable tech companies generate positive cash flow, and burn rate becomes less relevant for them. Additionally, burn rate analysis is less useful for companies in very early stages where there’s so much uncertainty that any projection is essentially guessing. At that stage, you’re betting on the team and market more than the financials.

This framework is most powerful for growth-stage companies — those with meaningful revenue but not yet profitable, where the gap between what’s coming in and what’s going out is still significant.

Conclusion

Burn rate isn’t sexy. It doesn’t make for exciting headlines or viral social media posts. But it’s the metric that will tell you whether a company survives long enough to fulfill its promise. Growth can hide a multitude of sins. Burn rate exposes them.

The next time you’re evaluating a tech investment, start with the cash flow statement. Calculate the net burn. Figure out the runway under pessimistic scenarios. Ask what the company is actually purchasing with that cash. And if the numbers don’t make sense, trust the numbers — not the vision.

The best investors I’ve known are deeply skeptical of companies that need to keep raising capital to survive. They’re looking for businesses that could technically survive on their own economics if necessary, even if they choose to raise capital to grow faster. That optionality is what a healthy burn rate provides.

If you’re serious about investing in tech companies, build burn rate analysis into your due diligence process every single time. It won’t make you popular with founders who want to talk about nothing but growth. But it will save you from some of the most painful investment losses. The market has a way of punishing companies that run out of cash, and it rarely warns you first.